Master Limited Partnerships: exempt from corporate taxation, dominated by oil and gas industry

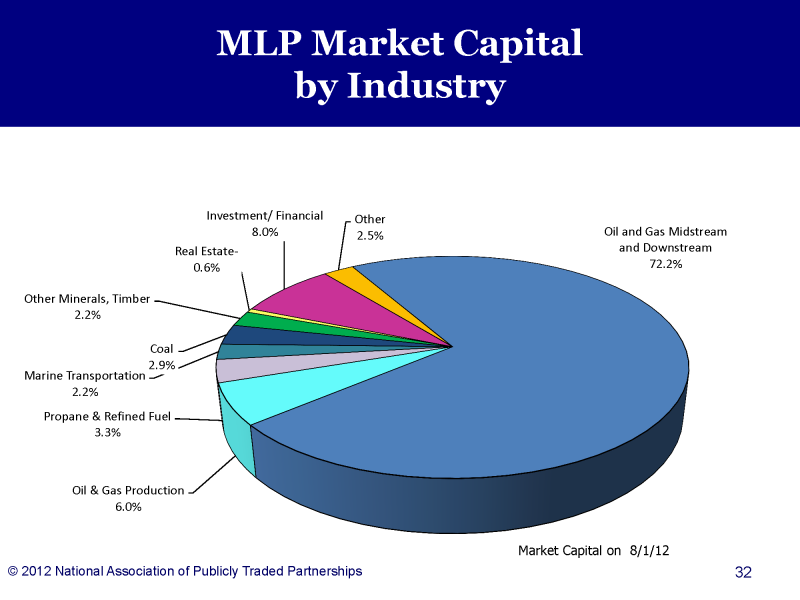

Master Limited Partnerships (MLPs) are a special corporate form, used primarily by natural resource industries. They enable firms to both raise capital on public equity markets and to pay zero corporate income taxes. MLPs deserve far more scrutiny as energy subsidies than they have received to date. Although the US Energy Information Administration (EIA) excluded them from their most recent study of US energy subsidies on the grounds that other industries also benefit (so the subsidies are not "energy-specific"), EIA's logic is weak. Based on data compiled by the National Association of Publicly Traded Partnerships in August 2012, roughly 87% of the total market capitalization of the MLP sector was associated with fossil-fuel related activity. That's pretty focused.

And the dollars look to be large -- between $5 and $15 billion/year in revenue losses, funds that either increase our deficit or have to be made up through higher taxes on other taxpayers. More precise review of data on specific MLPs would be needed to tighten this range. But even at the low end, tax subsidies through MLPs alone generate higher subsidies to fossil fuels than everything else that EIA counted combined. Let's just say that the government's subsidy figures are highly sensitive to which policies they ignore.

With enormous pressure on Congress to identify ways to boost revenues and reduce economic distortions from the tax code, stripping the tax exemption of MLPs seems a great place to look. Of course the industry will lobby heavily to protect their subsidy; it always does. But elimination is still good public policy. In fact, were the industry to argue that the world will end if MLP tax treatment changes, we can point out that Canada has already traveled this path. In 2006, Canada eliminated preferential tax treatment for their energy investment trusts, a corporate structure modeled on, and analogous to, MLPs. And the oil and gas industry did not disappear.

The remainder of this blog is extracted from a more detailed review I did on subsidies that the Romney presidential campaign forgot when it discussed energy subsidies.

Escaping corporation taxation entirely: Master Limited Partnerships

With all of the talk this campaign season about reducing income tax burdens on small business, it is easy to forget that an ever higher percentage of small businesses (and many larger ones) are adopting corporate forms that escape corporate income taxes entirely. This includes sub-S corporations, partnerships, and limited liability corporations. As a result, the share of national income paid from corporate income taxes has dropped from nearly 30% in the 1950s to less than 11% for the period 2000-2009.[1] But one group of enterprises - those raising capital on public equity markets - must generally still use corporate forms that pay corporate taxes.

One glaring exception is publicly-traded partnerships (PTPs), also known as Master Limited Partnerships (MLPs). Under special rules, this group of companies can both raise capital on public markets and bypass corporate income taxes entirely. Tax liabilities (and enterprise-related subsidies) pass directly out to the partners' individual tax returns. MLPs don't make up a huge chunk of listed firms on the stock market. But within the tax favored MLP universe, oil and gas companies dominate, including a new one focused on fracking sand.

One other sector able to use the MLP approach is also relevant to this debate: private equity firms. If Bain Capital (the firm that Mr. Romney founded) wanted to go public so partners could cash in their built-up equity, they would likely become an MLP. Blackstone and KKR, two large private equity firms, have already done so.

Table: Avoided taxes on oil and gas MLPs alone exceed totals subsidies DOE attributed to the sector

$293b/yr | Market capitalization of fossil fuel-related MLPs, as of August 2012.[2] The MLP corporate form allows many oil and gas operations to both raise capital on public stock markets and pay no corporate-level income taxes. |

$20-56b/yr | Estimated income generated by fossil fuel MLPs, based on reported yields. This income entirely escapes corporate taxation.[3] |

$5-15b/yr | Estimated tax savings to fossil fuel sector from using an MLP relative to a standard corporation, based on assumptions on tax rates by the National Association of Publicly Traded Partnerships. |

87% | Share of all MLPs, by market capitalization, in the fossil fuel sector. |

$0 | Subsidies associated with MLPs that the US Energy Information Administration captures in its evaluations, excluding it on the basis that "the tax treatment of PTPs is not exclusive to the energy sector."[4] |

1.8 - 5.4 | Tax subsidy to fossil fuel MLPs as a multiple of all subsidies to oil and gas EIA counted in its 2011 analysis. |

[1] Chuck Marr and Brian Highsmith, "Six Tests for Corporate Tax Reform," Center for Budget and Policy Priorities, 24 February 2012.

[2] National Association of Publicly Traded Partnerships, "Master Limited Partnerships 101: Understanding MLPs," August 2012.

[3] Low-end assumes a yield of 6.7%, the average of fossil-fuel-related MLPs based on MLPs listed on the Yield Hunter website with additional data from Google Finance. High-end estimate is from Telis Demos and Tom Lauricella, "Yield-Starved Investors Snap Up Riskier MLPs," Wall Street Journal, 16 September 2012.

[4] U.S. Energy Information Administration, Direct Federal Financial Interventions and Subsidies in Energy in Fiscal Year 2010, 2011, p. x.