The Joint Committee on Taxation of the US Congress has gradually posted many of its publications going back as early as 1926. Special tax rules for natural resources were a focus of JCT's attention even in its earliest days. By the mid-1920s, standard cost depletion had already been jettisoned for discovery value. Under cost depletion, taxpayers could write off what they'd invested in the mining property. Discovery value depletion introduced subsidization, as it allowed the write off of the value of minerals at the time of discovery, even if that value was more than the investment (as it normally would be, else the mine would be losing money). The discovery approach proved difficult to implement because the minable reserves couldn't always be assessed ahead of time, so the tax code shifted to percentage depletion, allowing 27.5% of the gross value of oil and gas to be written off from taxes each year. JCT was concerned about this from the outset:

The text below has a refreshing honesty, particularly in comparison to the bland bureaucratic language that pervades government documents today. The note to the in-process study reads:

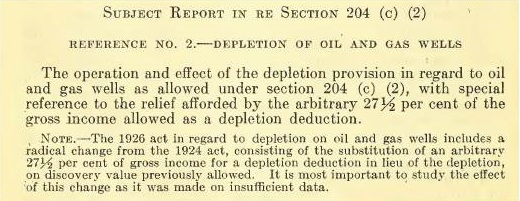

The 1926 act in regard to depletion on oil and gas wells includes a radical change from the 1924 act, consisting of the substitution of an arbitary 27 1/2 per cent of gross income for a depletion deduction in lieu of the depletion, on discovery value previously allowed. It is most important to study the effect of this change as it was made on insufficient data.

Rates are lower, and the largest of oil firms can no longer claim the subsidy. But the 1926 study, and however many more followed it, have never been sufficient to kill this tax break entirely. It remains a significant subsidy to oil and gas today.

The cover page of the JCT report is below. It can be read in full here.