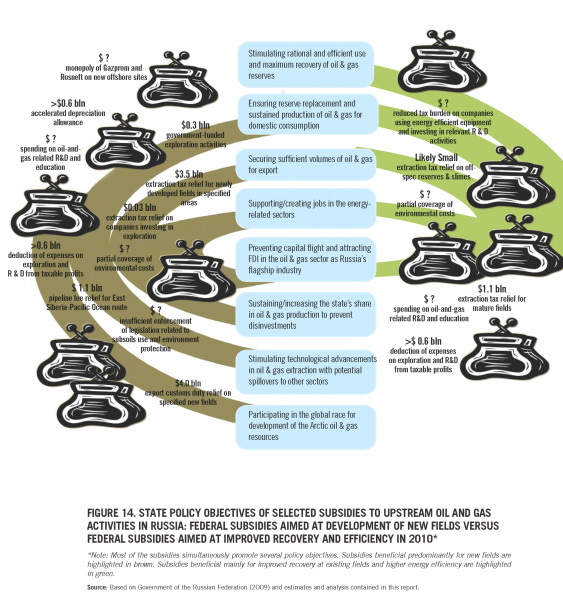

The Tax Foundation has penned a number of posts on the Section 199 Domestic Manufacturing Tax Deduction and the oil and gas industry. This subsidy allows companies to deduct up to 9 percent of their net income from domestic manufacturing activities, in the process bringing down their overall corporate tax rate.

The Tax Foundation agrees that the provision is a subsidy in general, and that more industry-neutral methods to bring down general corporate tax rates would be less distortionary. Their critique of removing the tax break independently for the oil and gas sectors is twofold: that eliminating the subsidy to oil and gas would be ineffective in meeting environmental objectives, since market prices won't change; and that singling out this industry alone amongst all manufacturers is arbitrary and unfair.

Impact of subsidy reform on energy markets. The question of how eliminating a particular subsidy provision will alter market prices is always a tough one. Oil is widely traded, and the US is not a low-cost producer. Thus, any cost increases from subsidy removal on the domestic market risk being competed away through increased imports, resulting in no change in price signals to consumers. There are a handful of relevant responses here:

First, natural gas is not so widely traded, and therefore domestic price increases from subsidy removal are more likely to flow through to domestic pricing and demand patterns. This is particularly true with gas moving to a marginal supplier position in power markets following fracking-related reductions in natural gas prices.

Second, focusing on the short-term impact of removing any single subsidy will inherently understate the benefits of broadscale subsidy reform. Even if domestic equilbrium prices don't change immediately, subsidy removal often affects the structure of supply -- and sometimes in quite beneficial ways. Removal of coal subsidies in the UK led to a significant increase in the share of cleaner natural gas in the power sector, for example. Similarly, if countries stop subsidizing higher-cost sources of extraction, such as through royalty relief or special tax breaks for remote or less lucrative formations, alternative ways to provide energy services have a much better chance of gaining a market foothold.

Third, the removal of groups of subsidies rather than a single one (basically what the Obama administration is trying to do in support of its G20 fossil fuel subsidy phase-out pledge) makes impacts on pricing and demand patterns much more likely. It is important to remember that the US also subsidizes foreign oil production through the tax code, provision of subsidized credit, and oil security services. Cutting all of the subsidies to both domestic and foreign production at once would be much more likely to affect domestic prices and inter-fuel substitution than limiting reform to the domestic industry only. A related issue involves subsidies to oil and gas that arise through insufficient user fees. The Strategic Petroleum Reserve, the inland waterway system (used heavily to move bulk coal and oil), and the highway system all have either no user fees at all or fees too low to allow the services to break-even (even on a non-profit, no return-on-investment basis). Because these fees hit a large portion of domestic oil consumption, they are harder to bypass by switching suppliers. Cost recovery for SPR, for example, could simply be added to the federal motor fuels excise tax. The harder the fees to bypass, the more likely we'll see appropriate price signals to the end-user.

Is targeting oil and gas for section 199 exclusion arbitrary? The second main line of criticism put forth by the Tax Foundation is that removing the section 199 credit only for oil and gas is arbitrary and unfair. They point out that many other industries continue to get it, and that some of those industries (e.g., asphalt layers) also contribute to the fossil fuel reliance that the Administration is targeting through excluding the oil and gas sector.

The examples of related industries that get to keep the breaks miss what I think is a key problem with the tax credit: what constitutes "manufacturing"? If you invest in drilling rigs, oil refineries, and pipelines, that is as much manufacturing as making the asphalt for the roads or the vehicles that drive on them.

But the uranium ore, oil, gas or coal that is pulled from the ground has not been "manufactured." Rather, it is part of a natural resource endowment that our country and its citizens are fortunate to have, and and that we have a responsibility to manage wisely. So too with the water used in the extraction process or to irrigate the crops, and that is often degraded and polluted in the process. Is pulling water from acquifers "manufacturing"? The pipes and pumps may be, but the water itself is not.

Yet in these, and likely many other cases, the endowment value of the resource itself is being counted as part of the domestic production gross receipts that are used to calculate the value of the tax subsidy. Here is the specific Section 199 language of concern (emphasis added), courtesy of the Cornell Law Library:

4) Domestic production gross receipts

(A) In general The term “domestic production gross receipts” means the gross receipts of the taxpayer which are derived from—

(i) any lease, rental, license, sale, exchange, or other disposition of— (I) qualifying production property which was manufactured, produced, grown, or extracted by the taxpayer in whole or in significant part within the United States, (II) any qualified film produced by the taxpayer, or (III) electricity, natural gas, or potable water produced by the taxpayer in the United States...

While it may well make sense to kill the entire section 199 subsidy, making the endowment value of extracted natural resources ineligable would be a good start.