It's been a rough few months for nuclear power, with the bankruptcy of Westinghouse, the US nuclear arm of Toshiba; continued cost escalation at both US reactor projects and the UK's Hinkley C; and the decision on Monday to abandon two in-process reactors at the V.C. Summer site in South Carolina. This is clearly an escalation of bad news, but the problems have been coming on a regular schedule for over a decade at this point. There's been a continuous economic bleed since the heady days in which a nuclear "renaissance" was to usher in a wave of clean baseload and dispatchable power. If not quite too cheap to meter, new nukes were still sold as being a good deal for ratepayers and for the country.

Big projects being built with other people's money always warrant careful and skeptical review

This was not a story I ever believed. Massive historical cost overruns in the US on reactor projects; all sorts of delivery problems on recent European ones; rising competition from natural gas; sharply falling costs for wind, solar and power storage; and the significant unresolved long-tail challenges of accidents, waste management, and decommissioning all contributed to a tough-sell to investors for an industry that produces what is, at its most basic, a commodity.

Then there is the fact that when companies spend other people's money they tend to be way less focused on good decisions. They certainly don't want to fail, but they often take more risks, pay less attention to cost control, and less carefully vet their assumptions on market trends and alternative solutions. All told, the headwinds impeding a broad industry turnaround seemed very strong.

Some subsidies are easy to see and understand: cash from the government goes to a firm to spend in a pre-determined way. In contrast, nuclear subsidies can be both fiendishly complex and eye-wateringly boring. Despite their importance in skewing the direction of energy markets, this combination of features makes them quite hard to explain to more general audiences. That changes, of course, when there are bankruptcies and members of this general audience begin to lose lots of money (as is now happening in South Carolina). Suddenly, they care about the details and want to change them. By then, however, it is usually too late.

Back in 2005, and in an effort to make the subsidies more accessible, I developed a slide pack promoting a satirical new industry association called the NuSubsidies Nuclear Consortium. The name was in reference to the real NuStart initiative, an effort to restart the industry that included many of the largest players at the time.

NuSubsidies was focused on maximizing use of the public trough. It had the tagline "Where the Taxpayer is our Favorite Investor," and it's strategy was to boost the financial returns for reactor project developers using its patented Policy Enhanced Investment, or PEI. The PEI approach shifted all sorts of operational and financial risks away from investors onto taxpayers, while retaining the full share of profits from any successes.

Although many of the links have likely gone dead over the past 12 years, it is striking how many of these core satirical strategies have played out in reality.

Nuclear Energy Institute, good times ahead

The Nuclear Energy Institute (NEI) was leading the charge touting nuclear as energy market salvation. A decade ago, they were working hard not only on public subsidy front -- a continued area of focus for the industry's largest trade association -- but also on the private financing side as well. There was a belief, or at least a hope, that under the right conditions private money would flood into new reactor projects, restarting supply chains and rebuilding an industry in which both the specialists and the equipment were rapidly aging.

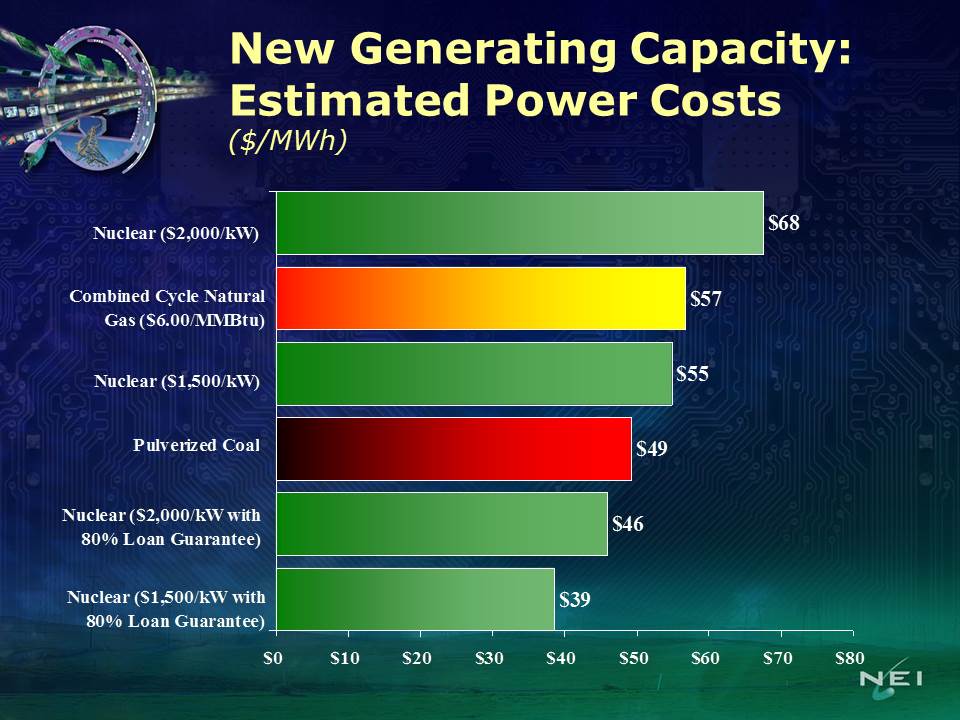

The slide below is from NEI CEO Frank Bowman's Briefing for the Wall Street Utility Group on September 22, 2005. Only Bowman himself knows if he even believed the numbers back in 2005, but they sure painted a rosy picture of the technology despite a half-century of prior fiscal problems, cost overruns, and project abandonments. Look how positively competitive nuclear looks, even against natural gas. NEI pegged the highest nuclear cost in their scenarios at $68/MWh, and combined cycle natural gas at $57/MWh.

Turns out these estimates were not very accurate. EIA's most recent projections have similar values for natural gas, but estimate advanced nuclear at more than $96/MWh, more than 40% higher than NEI's old high estimates. Further, the EIA projections are based on the two US projects ongoing at the time of their work, and their estimates show a lower levelized cost than reality because they seem to embed significant financing subsidies (including CWIP and and large loan guarantees) within their cost models. Further, there is nobody who believes cost escalation is finished at the one remaining US project (Vogtle in Georgia), and this will play out in future EIA estimates. For another benchmark, taxpayers in the UK are guaranteeing a price of £92.50/MWh (roughly $122/MWh) at the Hinkley Point C nuclear project. This is twice the price of power in Britain.

Bowman's slide is also interesting in that it quantifies large financial benefits from federal loan guarantees. Only once political opposition to the loan guarantees started to mount did the industry begin claiming (often concurrent with grabbing the subsidies) that they didn't really need the guarantees and they weren't worth very much.

While the VC Summer project did not tap into the federal loan guarantee program (relying instead on fixed price contracts with Westinghouse that ultimately drove that supplier into bankruptcy), executives had been scrambling in recent months for a bailout from Uncle Sam. Apparently, DOE did offer them a loan, but they wanted more financial support, and for it to convert into a grant if they ran into continued trouble. To the credit of the Trump Administration, DOE did not offer it.

A few years ago, Taxpayers for Common Sense compiled a summary of Southern Company (the largest partner in the massively expensive and only remaining nuclear new build in Georgia) executive quotes claiming they didn't need a massive federal loan guarantee to move forward. This was something I had hoped the government would have taken Southern up on -- why give subsidized money to a firm that says that they don't need it, particularly when key aspects of the decision making for these loans were done on private emails that do not seem ever to have been released during FOIA requests?

But rising costs at Vogtle make abandonment of the project there more likely as well. Such an outcome would dump up to $8.3 billion in loan liability onto federal taxpayers. While former DOE Secretary Ernest Moniz clearly wants nuclear to make it in the US (he was co-chair of the study group that produced MIT's very detailed review of nuclear power in 2003), his decision to move forward with the loan guarantee despite company statements they didn't need it will be a large stain on his legacy should Vogtle become insolvent.

NEI promoted very low nuclear power costs in 2005

Endless Summer: Costs of abandonment in South Carolina

On July 18th, Mark Cooper, a Senior Fellow at the Vermont Law School, submitted a detailed brief on the costs of the Summer 2 and 3 reactors and estimated that abandoning the project now would save ratepayers billions of dollars. Conducted on behalf of environmental NGOs Sierra Club and Friends of the Earth, the material provided background detail for a complaint to be filed with the South Carolina Public Services Commission in October. Cooper had done a similar review back in 2012, also finding that the completed plant would be unlikely to produce power competitively, and that terminating the project despite sunk costs would be economically rational.

On July 27th, Toshiba, the parent company of bankrupt reactor manufacturer Westinghouse, agreed to pay a $2.2 billion settlement for the two reactors whether or not they were ever completed. This gave the management team on the Summer projects more latitude to bail, and bail they did. On July 31st, the two owners of the Summer 2 & 3 project South Carolina Electric & Gas Co. (SCE&G) and publicly-owned Santee Cooper announced they were abandoning the project after roughly $9 billion invested. They were less than 40% complete and years behind schedule.

Power demand in the region was flat and natural gas prices remained low. Costs to complete were now projected at $25 billion, more than double the initial $11.5 billion estimate -- and that is with significant embedded subsidies by funding a portion of the projects in ratepayers' bills under South Carolina's Baseload Review Act. The Act allowed the utilities to charge customers for the new construction before the plants came on line, operating like an interest-free loan.

Santee Cooper raised rates five times to cover rising construction costs being passed through to its customers. Nearly 20% of SCE&G's customer bills were due to these costs as well, with $1.4 billion collected thus far through nine rate increases over roughly ten years.

Of the $9 billion spent, nearly $7 billion is likely to be put through to ratepayers though the plant is unlikely to ever be completed. The remaining $2.2 billion has been pledged by Toshiba under the recent deal. While Toshiba remains solvent, it is under significant financial strain and may not be able to make good. Further, news coverage discussing the Toshiba payment say it could be used for relief to ratepayers though make no firm commitment to do so.

And while the Summer project seems dead for the foreseeable future, it will indeed be an endless summer for ratepayers. Surcharges to fund the construction are likely to continue hitting their bills for the next 60 years.

Unheeded warnings from the past

As reported in the Charlotte Business Journal

PSC Chairman Swain Whitfeld told the SCANA group [the parent company of SCE&G] “this commission was blindsided ... by this news” that Summer would be abandoned. “This is going to shatter lives, hopes, and dreams, in Fairfeld County (where the project was being built) and in the state of South Carolina,” he said.

But there have been warning signs for years, and hopefully the ratepayers in the VC Summer district will comb through the PSC' history on the project to see why this outcome would have come as a surprise. Back to Mark Cooper here, and also to former NRC Commissioner Peter Bradford. (In full disclosure, I know both of them and respect their work).

Cooper has been writing about cost escalation in the nuclear renaissance for the entire period of this supposed rebirth. Bradford has long focused on the mechanisms used to shift funding and performance risks to ratepayers through various permutations of construction work in progress rules.

Here's a few related tidbits from Bradford's testimony before the South Carolina PSC in 2008. Though it related to Duke Power (which was planning its own reactor in SC), many of the issues are the same with the Summer plants:

Q. WHY DOES SOUTH CAROLINA'S STATUTORY FRAMEWORK CONFER AN "EXTRAORDINARY BENEFIT" ON DUKE?

A. Because it allows the decision to construct the proposed nuclear unit to be deemed prudent based on a review conducted long before events point to anything that has actually gone wrong. On the basis of this necessarily incomplete review, Duke will be well on the road to being able to recover a very substantial portion of its costs before the plant ever operates. No other type of large industrial facility enjoys this capability. A paper mill or an oil refinery must produce products at a competitive price to recover their costs. Indeed, even a nuclear power plant built in restructured markets (where cost recovery depends on participation in a power market) cannot recover costs until it produces kilowatt hours at a competitive price.

….

Q. WHAT IS THE RELATIONSHIP BETWEEN THE POINTS THAT YOU HAVE MADE AND DUKE'S RETURN ON EQUITY?

A. Shifting risk from investors to customers does not produce real savings. It lowers the cost of capital used in building the plant by increasing customer exposure to costly events that might otherwise have been borne by investors. If any of these events occur, the customers will pay for them, and this risk offsets any savings from the reduced cost of capital. The Commission should at least lower Duke's return on equity in order prevent the injustice of having customers pay investors as if they were bearing the risks that have in fact been shifted to the customers.

Cooper's positions on nuclear costs and competitiveness seem to have been far more on target than those promoting the industry as well. Not surprisingly, however, the industry thinks things are just fine. Here's NEI's David Bradish on CWIP, Cooper, and Bradford in 2013. Bradish is an articulate, albeit partisan, explainer of all the reasons why subsidies to nuclear aren't really subsidies.

Because the interest on debt and return on equity are being paid each year, these carrying costs are not accumulating as they would in the absence of CWIP, to be recovered when the plant begins operation. Because these costs, like all debt, compound over time, the quicker they are paid, the less they build up. When ratepayers pay these carrying costs while the plants are under construction, customers will save substantial sums over the life of the units.

But this isn't really a savings; it is a trade. Take money from customers now, pay them no interest, and as a result the amount you charge them later will be less. But what if your customer is in debt, and has higher credit card bills (at very high interest rates)? Because SCG&E is charging him 18% more per month for his electricity, his consumer debt is higher, and he is clearly worse off. Or what if the plant is never completed, so the customer has just fronted money for ten years, for free, with no recourse?

More from Bradish:

Cooper’s paper [an earlier one] claims that “ratepayers are on the hook” and taking all the risk of building a nuclear plant because of CWIP. Apparently, Cooper does not understand how utilities build and recover the costs of power plants in regulated states.

Just because many regulated states allow CWIP doesn't mean that it isn't a subsidy. Indeed, it is one reason that no new reactors were getting built in merchant power states. CWIP is a financing strategy that is lucrative for utilities, particularly those building long-gestation, high capital cost projects and looking for places (other than their shareholders) to shift the risks of cost escalation.

Cooper and his fellow anti-nuclear critics contend that CWIP allows utilities to collect costs without having to build the plant. Cooper’s paper claims that they can get halfway through the project, cancel it, and then collect the incurred costs of construction from ratepayers without having to pay anything. This is of course an erroneous view of how states govern projects.

Wow, hold on David. Isn't that exactly what is going on now in South Carolina? Yes, there might sometimes be a prudence review, so CWIP isn't always a blank check. But it is (a) a subsidy even when the plant is completed; and (b) has often been modified such that there is much less prudence review (e.g., with "super-CWIP" where money is recoverable just by the utility demonstrating that it has been spent). And just to be clear, the customers expecting a refund on their advance funding of a new nuclear albatross shouldn't count on it.

Bradish:

CWIP is not new and, as shown above, allows customers the benefit of lower electricity costs from a reliable, affordable, emission-free source of power that can last 60 to 80 to 100 years.

A few final points. First, percentage depletion for oil, gas, and coal is even older than CWIP, but is still a subsidy, still distorts market choices, and should still be eliminated. Age has nothing to do with CWIP being a subsidy either; it is simply an old subsidy. Second, these schemes shift capital risks from the investors to ratepayers, and an important side-effect can be that they skew markets to take on more capital-intensive approaches than would otherwise occur. This is a negative policy outcome. Third, while it is certainly true that running any piece of capital equipment for longer reduces the capital cost per unit of production, it seems reckless for Bradish to claim we have any reactor technologies capable of lasting 80 or 100 years in a safe manner.

Facing cost pressures and eroding market position? Time for a bikini contest

Because nothing screams technical competence in an industry where mistakes can spread radioactivity over a wide region than a bikini contest:

Power generation conglomerate CEZ had 10 bikini-clad high school graduates pose in a cooling tower of its Temelin nuclear power plant, which was briefly closed for maintenance.

It then asked Facebook users to vote for their favorite, with the most popular winning a 14 day internship at the plant.

In a press release CEZ likened the photoshoot to its previous cultural enrichment programs, such as hosting the Bohemian Philharmonic at the plant in South Bohemia. The release said the experience was greatly enjoyed by the girls, who were required to wear hard hats and enclosed shoes at all times.

Yeah, really. After an uproar on social media, the plant eventually apologized.