It's been a rough few months for nuclear power, with the bankruptcy of Westinghouse, the US nuclear arm of Toshiba; continued cost escalation at both US reactor projects and the UK's Hinkley C; and the decision on Monday to abandon two in-process reactors at the V.C. Summer site in South Carolina. This is clearly an escalation of bad news, but the problems have been coming on a regular schedule for over a decade at this point. There's been a continuous economic bleed since the heady days in which a nuclear "renaissance" was to usher in a wave of clean baseload and dispatchable power. If not quite too cheap to meter, new nukes were still sold as being a good deal for ratepayers and for the country.

Big projects being built with other people's money always warrant careful and skeptical review

This was not a story I ever believed. Massive historical cost overruns in the US on reactor projects; all sorts of delivery problems on recent European ones; rising competition from natural gas; sharply falling costs for wind, solar and power storage; and the significant unresolved long-tail challenges of accidents, waste management, and decommissioning all contributed to a tough-sell to investors for an industry that produces what is, at its most basic, a commodity.

Then there is the fact that when companies spend other people's money they tend to be way less focused on good decisions. They certainly don't want to fail, but they often take more risks, pay less attention to cost control, and less carefully vet their assumptions on market trends and alternative solutions. All told, the headwinds impeding a broad industry turnaround seemed very strong.

Some subsidies are easy to see and understand: cash from the government goes to a firm to spend in a pre-determined way. In contrast, nuclear subsidies can be both fiendishly complex and eye-wateringly boring. Despite their importance in skewing the direction of energy markets, this combination of features makes them quite hard to explain to more general audiences. That changes, of course, when there are bankruptcies and members of this general audience begin to lose lots of money (as is now happening in South Carolina). Suddenly, they care about the details and want to change them. By then, however, it is usually too late.

Back in 2005, and in an effort to make the subsidies more accessible, I developed a slide pack promoting a satirical new industry association called the NuSubsidies Nuclear Consortium. The name was in reference to the real NuStart initiative, an effort to restart the industry that included many of the largest players at the time.

NuSubsidies was focused on maximizing use of the public trough. It had the tagline "Where the Taxpayer is our Favorite Investor," and it's strategy was to boost the financial returns for reactor project developers using its patented Policy Enhanced Investment, or PEI. The PEI approach shifted all sorts of operational and financial risks away from investors onto taxpayers, while retaining the full share of profits from any successes.

Although many of the links have likely gone dead over the past 12 years, it is striking how many of these core satirical strategies have played out in reality.

Nuclear Energy Institute, good times ahead

The Nuclear Energy Institute (NEI) was leading the charge touting nuclear as energy market salvation. A decade ago, they were working hard not only on public subsidy front -- a continued area of focus for the industry's largest trade association -- but also on the private financing side as well. There was a belief, or at least a hope, that under the right conditions private money would flood into new reactor projects, restarting supply chains and rebuilding an industry in which both the specialists and the equipment were rapidly aging.

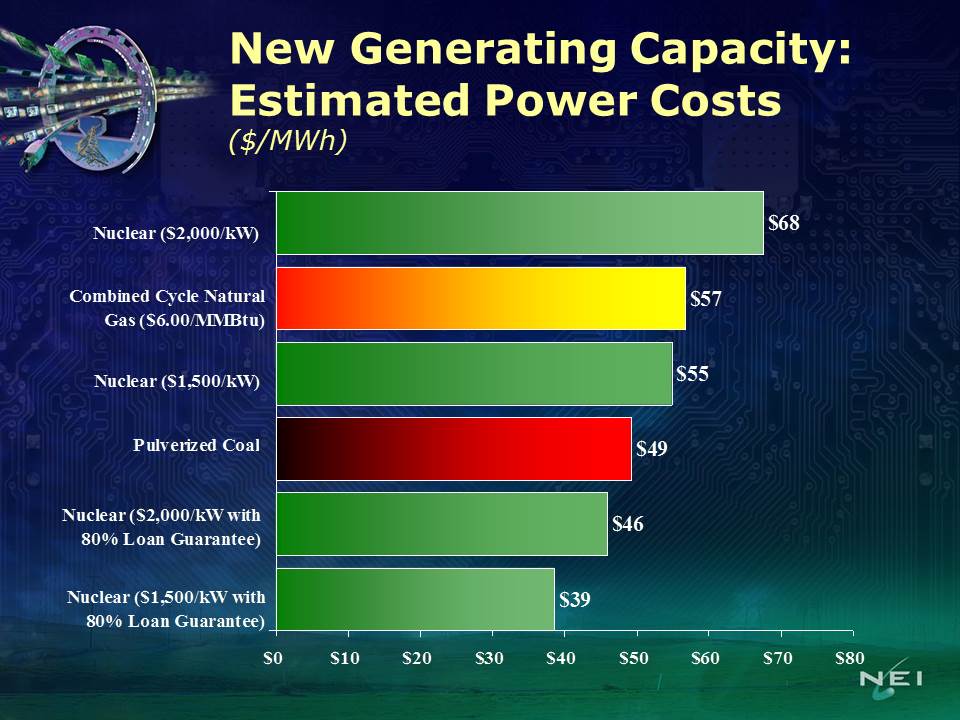

The slide below is from NEI CEO Frank Bowman's Briefing for the Wall Street Utility Group on September 22, 2005. Only Bowman himself knows if he even believed the numbers back in 2005, but they sure painted a rosy picture of the technology despite a half-century of prior fiscal problems, cost overruns, and project abandonments. Look how positively competitive nuclear looks, even against natural gas. NEI pegged the highest nuclear cost in their scenarios at $68/MWh, and combined cycle natural gas at $57/MWh.

Turns out these estimates were not very accurate. EIA's most recent projections have similar values for natural gas, but estimate advanced nuclear at more than $96/MWh, more than 40% higher than NEI's old high estimates. Further, the EIA projections are based on the two US projects ongoing at the time of their work, and their estimates show a lower levelized cost than reality because they seem to embed significant financing subsidies (including CWIP and and large loan guarantees) within their cost models. Further, there is nobody who believes cost escalation is finished at the one remaining US project (Vogtle in Georgia), and this will play out in future EIA estimates. For another benchmark, taxpayers in the UK are guaranteeing a price of £92.50/MWh (roughly $122/MWh) at the Hinkley Point C nuclear project. This is twice the price of power in Britain.

Bowman's slide is also interesting in that it quantifies large financial benefits from federal loan guarantees. Only once political opposition to the loan guarantees started to mount did the industry begin claiming (often concurrent with grabbing the subsidies) that they didn't really need the guarantees and they weren't worth very much.

While the VC Summer project did not tap into the federal loan guarantee program (relying instead on fixed price contracts with Westinghouse that ultimately drove that supplier into bankruptcy), executives had been scrambling in recent months for a bailout from Uncle Sam. Apparently, DOE did offer them a loan, but they wanted more financial support, and for it to convert into a grant if they ran into continued trouble. To the credit of the Trump Administration, DOE did not offer it.

A few years ago, Taxpayers for Common Sense compiled a summary of Southern Company (the largest partner in the massively expensive and only remaining nuclear new build in Georgia) executive quotes claiming they didn't need a massive federal loan guarantee to move forward. This was something I had hoped the government would have taken Southern up on -- why give subsidized money to a firm that says that they don't need it, particularly when key aspects of the decision making for these loans were done on private emails that do not seem ever to have been released during FOIA requests?

But rising costs at Vogtle make abandonment of the project there more likely as well. Such an outcome would dump up to $8.3 billion in loan liability onto federal taxpayers. While former DOE Secretary Ernest Moniz clearly wants nuclear to make it in the US (he was co-chair of the study group that produced MIT's very detailed review of nuclear power in 2003), his decision to move forward with the loan guarantee despite company statements they didn't need it will be a large stain on his legacy should Vogtle become insolvent.

NEI promoted very low nuclear power costs in 2005

Endless Summer: Costs of abandonment in South Carolina

On July 18th, Mark Cooper, a Senior Fellow at the Vermont Law School, submitted a detailed brief on the costs of the Summer 2 and 3 reactors and estimated that abandoning the project now would save ratepayers billions of dollars. Conducted on behalf of environmental NGOs Sierra Club and Friends of the Earth, the material provided background detail for a complaint to be filed with the South Carolina Public Services Commission in October. Cooper had done a similar review back in 2012, also finding that the completed plant would be unlikely to produce power competitively, and that terminating the project despite sunk costs would be economically rational.

On July 27th, Toshiba, the parent company of bankrupt reactor manufacturer Westinghouse, agreed to pay a $2.2 billion settlement for the two reactors whether or not they were ever completed. This gave the management team on the Summer projects more latitude to bail, and bail they did. On July 31st, the two owners of the Summer 2 & 3 project South Carolina Electric & Gas Co. (SCE&G) and publicly-owned Santee Cooper announced they were abandoning the project after roughly $9 billion invested. They were less than 40% complete and years behind schedule.

Power demand in the region was flat and natural gas prices remained low. Costs to complete were now projected at $25 billion, more than double the initial $11.5 billion estimate -- and that is with significant embedded subsidies by funding a portion of the projects in ratepayers' bills under South Carolina's Baseload Review Act. The Act allowed the utilities to charge customers for the new construction before the plants came on line, operating like an interest-free loan.

Santee Cooper raised rates five times to cover rising construction costs being passed through to its customers. Nearly 20% of SCE&G's customer bills were due to these costs as well, with $1.4 billion collected thus far through nine rate increases over roughly ten years.

Of the $9 billion spent, nearly $7 billion is likely to be put through to ratepayers though the plant is unlikely to ever be completed. The remaining $2.2 billion has been pledged by Toshiba under the recent deal. While Toshiba remains solvent, it is under significant financial strain and may not be able to make good. Further, news coverage discussing the Toshiba payment say it could be used for relief to ratepayers though make no firm commitment to do so.

And while the Summer project seems dead for the foreseeable future, it will indeed be an endless summer for ratepayers. Surcharges to fund the construction are likely to continue hitting their bills for the next 60 years.

Unheeded warnings from the past

As reported in the Charlotte Business Journal

PSC Chairman Swain Whitfeld told the SCANA group [the parent company of SCE&G] “this commission was blindsided ... by this news” that Summer would be abandoned. “This is going to shatter lives, hopes, and dreams, in Fairfeld County (where the project was being built) and in the state of South Carolina,” he said.

But there have been warning signs for years, and hopefully the ratepayers in the VC Summer district will comb through the PSC' history on the project to see why this outcome would have come as a surprise. Back to Mark Cooper here, and also to former NRC Commissioner Peter Bradford. (In full disclosure, I know both of them and respect their work).

Cooper has been writing about cost escalation in the nuclear renaissance for the entire period of this supposed rebirth. Bradford has long focused on the mechanisms used to shift funding and performance risks to ratepayers through various permutations of construction work in progress rules.

Here's a few related tidbits from Bradford's testimony before the South Carolina PSC in 2008. Though it related to Duke Power (which was planning its own reactor in SC), many of the issues are the same with the Summer plants:

Q. WHY DOES SOUTH CAROLINA'S STATUTORY FRAMEWORK CONFER AN "EXTRAORDINARY BENEFIT" ON DUKE?

A. Because it allows the decision to construct the proposed nuclear unit to be deemed prudent based on a review conducted long before events point to anything that has actually gone wrong. On the basis of this necessarily incomplete review, Duke will be well on the road to being able to recover a very substantial portion of its costs before the plant ever operates. No other type of large industrial facility enjoys this capability. A paper mill or an oil refinery must produce products at a competitive price to recover their costs. Indeed, even a nuclear power plant built in restructured markets (where cost recovery depends on participation in a power market) cannot recover costs until it produces kilowatt hours at a competitive price.

….

Q. WHAT IS THE RELATIONSHIP BETWEEN THE POINTS THAT YOU HAVE MADE AND DUKE'S RETURN ON EQUITY?

A. Shifting risk from investors to customers does not produce real savings. It lowers the cost of capital used in building the plant by increasing customer exposure to costly events that might otherwise have been borne by investors. If any of these events occur, the customers will pay for them, and this risk offsets any savings from the reduced cost of capital. The Commission should at least lower Duke's return on equity in order prevent the injustice of having customers pay investors as if they were bearing the risks that have in fact been shifted to the customers.

Cooper's positions on nuclear costs and competitiveness seem to have been far more on target than those promoting the industry as well. Not surprisingly, however, the industry thinks things are just fine. Here's NEI's David Bradish on CWIP, Cooper, and Bradford in 2013. Bradish is an articulate, albeit partisan, explainer of all the reasons why subsidies to nuclear aren't really subsidies.

Because the interest on debt and return on equity are being paid each year, these carrying costs are not accumulating as they would in the absence of CWIP, to be recovered when the plant begins operation. Because these costs, like all debt, compound over time, the quicker they are paid, the less they build up. When ratepayers pay these carrying costs while the plants are under construction, customers will save substantial sums over the life of the units.

But this isn't really a savings; it is a trade. Take money from customers now, pay them no interest, and as a result the amount you charge them later will be less. But what if your customer is in debt, and has higher credit card bills (at very high interest rates)? Because SCG&E is charging him 18% more per month for his electricity, his consumer debt is higher, and he is clearly worse off. Or what if the plant is never completed, so the customer has just fronted money for ten years, for free, with no recourse?

More from Bradish:

Cooper’s paper [an earlier one] claims that “ratepayers are on the hook” and taking all the risk of building a nuclear plant because of CWIP. Apparently, Cooper does not understand how utilities build and recover the costs of power plants in regulated states.

Just because many regulated states allow CWIP doesn't mean that it isn't a subsidy. Indeed, it is one reason that no new reactors were getting built in merchant power states. CWIP is a financing strategy that is lucrative for utilities, particularly those building long-gestation, high capital cost projects and looking for places (other than their shareholders) to shift the risks of cost escalation.

Cooper and his fellow anti-nuclear critics contend that CWIP allows utilities to collect costs without having to build the plant. Cooper’s paper claims that they can get halfway through the project, cancel it, and then collect the incurred costs of construction from ratepayers without having to pay anything. This is of course an erroneous view of how states govern projects.

Wow, hold on David. Isn't that exactly what is going on now in South Carolina? Yes, there might sometimes be a prudence review, so CWIP isn't always a blank check. But it is (a) a subsidy even when the plant is completed; and (b) has often been modified such that there is much less prudence review (e.g., with "super-CWIP" where money is recoverable just by the utility demonstrating that it has been spent). And just to be clear, the customers expecting a refund on their advance funding of a new nuclear albatross shouldn't count on it.

Bradish:

CWIP is not new and, as shown above, allows customers the benefit of lower electricity costs from a reliable, affordable, emission-free source of power that can last 60 to 80 to 100 years.

A few final points. First, percentage depletion for oil, gas, and coal is even older than CWIP, but is still a subsidy, still distorts market choices, and should still be eliminated. Age has nothing to do with CWIP being a subsidy either; it is simply an old subsidy. Second, these schemes shift capital risks from the investors to ratepayers, and an important side-effect can be that they skew markets to take on more capital-intensive approaches than would otherwise occur. This is a negative policy outcome. Third, while it is certainly true that running any piece of capital equipment for longer reduces the capital cost per unit of production, it seems reckless for Bradish to claim we have any reactor technologies capable of lasting 80 or 100 years in a safe manner.

Facing cost pressures and eroding market position? Time for a bikini contest

Because nothing screams technical competence in an industry where mistakes can spread radioactivity over a wide region than a bikini contest:

Power generation conglomerate CEZ had 10 bikini-clad high school graduates pose in a cooling tower of its Temelin nuclear power plant, which was briefly closed for maintenance.

It then asked Facebook users to vote for their favorite, with the most popular winning a 14 day internship at the plant.

In a press release CEZ likened the photoshoot to its previous cultural enrichment programs, such as hosting the Bohemian Philharmonic at the plant in South Bohemia. The release said the experience was greatly enjoyed by the girls, who were required to wear hard hats and enclosed shoes at all times.

Yeah, really. After an uproar on social media, the plant eventually apologized.

1) Reuters attributes sunk costs of German nuclear capacity to renewables. Michael Marriotte of NIRS flagged this one. In a recent post, he pointed out that $75 billion Reuters implied was associated with Germany's transition away from nuclear was actually "for decommissioning Germany's reactors and building a permanent radioactive waste dump." This is a sunk cost, and will need to be paid under any scenario. It is an open question, however, who will pay the tab. The Reuters piece calls to some potentially problematic utility restructuring now underway. Utility E.ON, for example, is spinning off its conventional power plants (i.e., the "good" assets) into a separate company -- leaving the closing nuke assets on their own. E.ON, as well as other German utilities, released statements saying that the residual nuclear firms had adequate assets to cover the costs of closure and decommissioning. The German government is not so sure. Billions will ride on which side is correct. I'm betting on cost overruns (the end-of-life fuel cycle costs for nuclear are not well tested) that get dumped on taxpayers. Some advance planning by the government to ensure a larger funding buffer, cost overage insurance, or continued access to related corporate entities in the case of shortfalls seems warranted.

2) Former nuclear reporter Matt Wald changes acronyms; bad optics, better money. For decades, most every story in the New York Times covering the nuclear power sector was written by Matt Wald. In December he took a buyout offer from the NYT to leave the paper; and in March he announced that he was taking a new position with the Nuclear Energy Institute (NEI). NEI is funded with nearly $50 million per year in fees from the nuclear industry, and serves as it main lobbying mouthpiece. This is lobbying in a policy-influencing kind of way rather than however federal law defines lobbying expenditures: the tax-exempt NEI lists formal lobbying expenditures at zero in its most recent tax filings (see PDF pages 16 and 17).

There is no question that being a reporter for conventional media is a tough business today. Pay was never particularly good, and old media companies remain under financial pressure from all sorts of new competitors. The economics of the move are obvious: Wald will take home a much bigger slug of cash working for the industry than he did reporting on it. In NEI's most recent tax filing, we can see that NEI President Marvin Fertel earned more than $3 million in direct and deferred compensation (Schedule J, Part II, PDF page 55). In contrast, Kevin Knobloch, president of the Union of Concerned Scientists (an organization which often counters NEI claims and proposals on nuclear energy), earned $301,000, roughly one-tenth of a Fertel (Schedule J, PDF page 30). Senior VP Alexander Flint, who worked on nuclear issues for Senator Pete Domenici prior to joining NEI, earned $771,000; and Wald's apparent new boss Scott Peterson, earned $584,000. Pay at the NYT was, umm, lower, according to Glassdoor and an article on top executive pay there in Slate.

But the move inevitably raises all sorts of questions, just as when a senior government regulatory official goes to work for the industries he or she previously regulated. How long was the move being considered? How did it affect the way the person previously did their job? Even if the new employer matches a policy or ideological perspective the new hire always had, what effect did that world view have on their prior work? Additional commentary here.

3) Back to the Future with former WNA economist Steve Kidd. Kidd penned a wide-ranging article on the benefits of nuclear energy and how to refocus its expansion in Nuclear Engineering International Magazine ("Is climate change the worst argument for nuclear," January 21, 2015). He argues that linking nuclear's growth primarily to its low carbon footprint is not working strategically, and advocates some other approaches. Specifically, Kidd suggests the industry focus on nuclear's clear-air benefits, since so many people are suffering from eggregious emissions of soot, particulates, SOx, NOx and ground level ozone so often linked to coal-fired electric power. No disagreement from me on the magnitude of the polution problem, but I fail to see much leverage in his strategy. It's not as though the nuclear industry is, or ever has, missed a chance to claim its benefits relative to coal. There is the current nuclear clean air campaign run by large nuclear firms; and big campaigns in decades past showing green skies, happy animals, and much assorted goodness arising from the use of nuclear. NEI's predecessor, the US Council for Energy Awareness, was a big funder of these campaigns (see ad). Further, all of the non-nuclear alternatives that are out-competing new reactors (natural gas, wind, solar, and efficiency) also eliminate or dramatically reduce these air emissions.

Kidd also clings to some of the common "blame-other-people for nuclear's problems approach." For example, he dislikes promoting environmentalists who have turned pro-nuclear because they have been "wrong" for so many years (i.e., by opposing nuclear) that they won't be trusted to be "right" now. And these people are the reason for nuclear's little cost problem:

Why on earth would one cosy up to the very people who killed your market in the first place because their foolish advocacy led to much higher costs.

This one is even better:

Nuclear has suffered far too much throughout its history from government intervention and controls. It now needs to sell itself on the grounds of cheapness, reliability, and security of supply. Nuclear advocates in the United States would do better if they could get the Department of Energy to back off the tangle of regulations put into place post-Three Mile Island, which have helped stall further development of nuclear there.

So in short, deregulate, silence critics, promote clean air. Hardly a business model and project delivery revolution. I am sure Wall Street will be impressed and the cash for new builds will flow in.

4) Gimme money or else I'll close the plant. Nuclear utilities in at least three states (NY, OH, and IL) are pushing for large operating subsidies or they say they will shut their plants. While nuclear plants have been touted as expensive to build but cheap to operate, these are examples where even the operating costs of plants that have already been paid off are too high to compete with alternatives. According to the Wall Street Journal, about half of the operating reactors in the US are in deregulated markets and therefore face the most acute pricing pressure. The Journal reports that about 1/3 are at risk of closure due to poor economics -- though if the utilities believe they might get cash bailouts, one must always assume the industry is overstating their pain.

The subsidies being requested are large. The Ginna reactor in NY is seeking more than $200 million per year. The bailout of three Exelon plants in Illinois is a cool $1.6 billion. Consumer groups and large industrial customers are not impressed, and oppose the bailouts. Note that these very same reactors have been subsidized in multiple ways for their entire existence. And they aren't opening their books even to verify they are losing what they claim they are losing, and SEC filings perhaps indicate they aren't actually losing money.

There are a host of related questions I'd love to see addressed on this issue. First, why is it not possible for the reactors to close voluntarily during periods of price weakness as other large industries do, and then restart if market conditions improve? We know this happens involuntarily, for example if reactor repairs take longer than expected -- so it is technically feasible. Voluntary shutdowns would preserve the capacity without government subsidy should the downturn really just be temporary -- while also keeping deregulated power markets competitive.

Second, as more reactors close, the insurance pool for nuclear accidents -- already way too low -- continues to drop linearly. How is the NRC planning for this? What steps are being taken to ensure even reactors that remain open have the financial capacity to pay their retrospective premiums under Price-Anderson, should the need arise?

5) Cost of MOX facility in Georgia close to $50 billion in current estimate. One final post on the problematic economics of the nuclear fuel cycle. The most recent cost estimate conducted by the National Nuclear Security Administration put the price to finish building and operate a mixed-oxide fuel facility at Savannah River in Georgia at $47.5 billion, according to a story in the Augusta Chronicle. This is much higher than previous estimates of life cycle costs (about $30 billion). Industry sources argue the newest estimate is too high, and there is no real problem.

The plant would convert surplus plutonium from weapons into materials that could be used to fuel nuclear power plants. Alternatives to dilute the plutonium to below-weapons grade, but not use in a reactor, appear to be less expensive. However, critics argue that downblending does not render the plutonium unusable for weapons and may not comply with US-Russian non-proliferation agreements.

NNSA has not released the report to the public because it contains "proprietary information." It is not classified however. Ed Lyman of the Union of Concerned Scientists has been tracking MOX cost escalation for years, and suggests the lack of a public release is driven more by political concerns over the price tag.

1) Poker, North Dakota style. Using a logic that only an industry trade association could understand, the US state of North Dakota has announced plans to close $50m/year in loopholes to oil and gas. Great! End subsidies that make no sense, such as lower taxes on low production "stripper" wells that have been exploited by nearby activities producing at much higher rates. But no reform is free, so the state officials are offering reduced tax rates on oil and gas in return. The rub: the reductions will cost the state an estimated $595m/year in new lost tax revenues, a mere 12x what they expect to get back from subsidy removal. In what world is giving away $12 in state revenues for each $1 you claw back considered good business? And it is not clear that even the 12:1 figure includes losses from new drilling incentives the state plans to put in place. Due to fracking, North Dakota is the country's second largest oil producer, after only Texas. This change is a big deal. For more information on how US states subsidize fossil fuels, go here. (Thanks to Ben Schreiber for the ND article link).

North Dakota's House rejected a measure Wednesday aimed at closing an exemption enjoyed by oil companies in exchange for lower tax rates.

The Republican-sponsored bill - one of the most contentious of the legislative session - also would have given the Three Affiliated Tribes a greater share of the taxes collected from reservation oil production.

Representatives crossed party lines and overwhelmingly defeated the measure 71-21.

Democrats, who are the minority in both chambers, have been especially critical of the measure, saying the proposed tax framework would have cost the state hundreds of millions of dollars in lost revenue over the next few years by lowering taxes on oil companies.

2) NEI thinks US nuclear export rules are too tight; looks to Russia as a model. The Nuclear Energy Institute's review of problems with our country's restrictive nuclear export regime is nothing if not bold. Here's their summary:

Compared to the nuclear export control regimes of Russia, Japan, ROK and France, the U.S. regime is, in many respects, more complex, restrictive and time-consuming to navigate and fulfill. Fundamental aspects of the U.S. export control regime were established over six decades ago – more than three decades prior to the creation of the Nuclear Suppliers Group (NSG).

During this time, the U.S. regime has evolved into a patchwork of requirements with layers of modifications. By comparison, the Russian, Japanese and ROK regimes are relatively modern and, in the case of the Japanese and ROK regimes, were recently amended to address post-9/11 nonproliferation concerns.

Now, I'm all in favor of looking to streamline the way government and business interact, but using Russia as a nuclear export model seems a sketchy strategy even for NEI. After all, Russian nuclear exports have been a bit of an issue for other parts of the US government for quite some time. But maybe that's the brilliance of the approach! Adopt Russian nuclear export rules, boost business for US nuclear suppliers (and NEI's members) by allowing quicker, broader nuclear exports; and force a ramping up of government efforts and funding through the State Department and the IAEA to deal with the political implications of expanding nuclear capabilities abroad. A job creation twofer!

3) Subsidy Cycles, UK style. Worried that your oil and gas operator didn't properly manage their environmental issues and taxpayers will be left paying reclamation costs? No need to be. Watch and learn from the UK - using subsidies to turn prior negligence into present opportunities! A Brownfields Tax Credit "rejuvenates" an "elderly" offshore field, allowing Enquest PLC to buy the Thistle field in the North Sea and for production to go on. No mention of what the government did wrong (poor oversight? inadequate bonding?) that resulted in the field being mismanaged by its prior operator in the first place; or of whether the government is trying to recapture reclamation costs (including the lost revenues due to the Brownfield subsidy) from that operator or its insurers. (Thanks to Ron Steenblik for the article link).

4) State subsidies for job creation: states are losing the bidding war.The Job Creation Shell Game, released in January, is a great review by Good Jobs First (a Washington, DC-based NGO) examining job poaching from one state to another. Not only do states routinely pay tax rebates to move old jobs from one state to another, but they then enter a process where large employers routinely threaten to move, extorting "retention" payments for staying put. Net job gains are small; net tax losses are big. And who do you think is left having to make up the lost tax revenues? Us, of course.

5) Relative scale: fossil fuel subsidies versus spending on international development. An interesting comparison of the scale of fossil fuel subsidies versus fast start climate spending by Oil Change International illustrates that nearly everywhere they looked, the subsidies to increased use of fossil fuels greatly exceeded the spending to start addressing the effects of consuming so many fossil fuels. Yes, some subsidies help the poor, and not all climate spending is efficient. But the gross comparison underscores how important it is for any effort to address climate change to incorporate ending subsidies as a central strategy.

1) Don't Prop up USEC. Henry Sokolski of the Nonproliferation Policy Education Center and Autumn Hanna at Taxpayers for Common Sense weigh in at the National Review Online on a proposed $2 billion dollar loan guarantee to finance new enrichment facilities for the United States Enrichment Corporation (USEC). USEC is the privatized residual of the government-run Uranium Enrichment Enterprise that ushered in the US nuclear era. In Another Solyndra: Ohio Republicans join the energy-subsidy racket, they argue that politics are leading the push of put taxpayer money at risk despite an extremely poor business case.

The business case should matter far more than it seems to in Washington. And this is so not just for each specific subsidy recipient, but also for how, in the aggregate, these interventions distort price signals and market structure overall.

With so much focus on solar subsidies, it is useful to point out that even if USEC doesn't get the guarantee in the end, they've already scored up to $300 million in federal money to "help USEC reduce the technical problems that forced DOE to reject USEC’s original application" for a Title 17 loan guarantee. That's bigger than the face value of many of the loan guarantees granted to renewable borrowers.

2) Anybody got a light? The effort to get the blaring light of fiscal conservative oversight now shining on Solyndra directed at least a tad towards the Vogtle nuclear deal proceeds on the dual tracks of litigation and legislation. Legal action by the Southern Alliance for Clean Energy (SACE) and Taxpayers for Common Sense to expose the terms of the loans continues, as DOE produced only heavily redacted documents in response the last FOIA request.

Of particular interest to SACE is information revealing whether company officials played an inappropriate role in shaping the terms of the loan guarantee. Based on the limited information produced, it appears that the power companies had to put almost no skin in the game, promising to pay a credit subsidy fee of possibly as little as 0.5 or 1.5 percent of the total loan guarantee.

House Democrats have been pushing for greater oversight legislatively as well, with a letter drafted by Rep. Henry Waxman (D-Calif.) and co-signed by Reps. Ed Markey (D-Mass.) and Diana DeGette (D-Colo.) to Chairmen Fred Upton (R-Mich.) and Cliff Stearns (R-Fla) of the House Energy and Commerce Committee. The letter notes that while they support a broadening of the Solyndra review to include 27 loan guarantees for renewable energy (something that has already been implemented), $10 billion in conditional guarantees to nuclear projects should also be included. This follows up on a similar push by letter co-signer Ed Markey last month.

In my book, this one is simple: if you aren't willing to look at potential conflicts of interest and corruption in all of the projects, don't call yourself a fiscal conservative.

3) Cash is cash, or don't cry when we invest your money abroad.Fisker Motors, recipient of a $529 million loan from the US DOE, is doing what any corporation does: it tries to find capital at the lowest possible cost and deploy that money however it sees fit to meet its own internal objectives. In this case, that means putting funds into manufacturing jobs abroad (or, per the input from Media Matters below, using the funding domestically to free up other funds to finance foreign manufacturing jobs). Oops.

On the other hand, as a major debtor to the firm, wouldn't taxpayers want Fisker to increase their chance of success as much as possible? Or, if you want to see electric vehicles enter the marketplace, wouldn't you want to maximize operational flexibility as well? I suppose that's the problem with having multiple objectives (is the loan for making jobs in the US or for trying to develop a new energy technology?).

Media Matters points out that the overseas construction was known prior to the loan guarantee being approved, implying this controversy is merely a manufactured issue. I disagree. The example underscores the core point that promoters of big federal subsidies too often ignore: in a global economy, building an industry from scratch doesn't mean it will all (or even mostly) be built here.

4) Risk is risk, or don't cry when bankruptcy or dilution come to call. The time for pricing risk is before you provide the credit. Happy talk about guarantees not really being subsidies (yes, we're talking about you, Dick Myers) should always be ignored by taxpayers and Congressmen alike.

A. The Belly-Up Club: Beacon Power becomes member number two. Flywheel producer (for bulk power storage) went belly-up today. Taxpayers were on the hook for $43 million. This, and Solyndra, will be good tests for the claims put forth by program promoters in years past that recoveries in bankruptcy will be substantial. Let's hope so.

Recoveries aside, expect more members in the Belly-Up Club soon. If we take the loan guarantee program to be what it really is -- investments with risks similar to venture capital or start-ups, expect failure rates of around 30-40%. If you expand the outcomes to include failure plus no return, we're up to 70-80% of the pool, according to Harvard Business School senior lecturer Shikhar Ghosh. Since Ghosh is talking private firms, and the incentive alignment within the Title 17 program between managers and the long-term performance of the firm is much worse, I'm expecting loss rates within the funded portfolio to be even larger absent big changes in the market (e.g., implementation of a large carbon tax).

B. Diluting the feds. Andrew Stiles raises concerns at the National Review Online that the restructuring of financing for Solyndra prior to its bankruptcy, a process that subordinated the Treasury's position in any subsequent bankruptcy, was illegal. He links to a series of e-mail chains on the restructuring, which are quite interesting in their own right:

Discussion of subordination starts on PDF page 14.

Page 21 notes that since July 2010 DOE was refusing to provide information on the Solyndra loan guarantee even to Treasury (which, of course, was backing the financing). This type of behavior underscores the concerns I had with program transparency and accountability back in 2007.

Page 22 indicates that Lazard was the firm providing independent review to DOE, perhaps of the original deal or perhaps only for strategic options for Solyndra at that point in time. There has been very little visibility on who the financial advisors to DOE have been on the Title 17 program, and therefore on the real or potential conflicts of interest these advisors may have. This is a problem.

Page 29 raises the intriguing possibility that investors may have been interested in keeping Solyndra alive longer to allow them to strip more assets from the firm (thereby reducing the government's collateral). Artificially high discounting of accounts receivable was one area mentioned.

While the lawyers will toil back and forth on the legality of subordination under the Title 17 authorizing legislation, to a great degree (and assuming there was no fraud or gross negligence within the government in the restructuring) it seems besides the point. If the government wants to do high risk investments, those investments go bad with surprising regularity. Any new money won't go in at the old terms. Either accept the risk of dilution, or don't play in the market.

d suggests the industry focus on nuclear's clear-air benefits, since so many people are suffering from eggregious emissions of soot, particulates, SOx, NOx and ground level ozone so often linked to coal-fired electric power. No disagreement from me on the magnitude of the polution problem, but I fail to see much leverage in his strategy. It's not as though the nuclear industry is, or ever has, missed a chance to claim its benefits relative to coal. There is the

d suggests the industry focus on nuclear's clear-air benefits, since so many people are suffering from eggregious emissions of soot, particulates, SOx, NOx and ground level ozone so often linked to coal-fired electric power. No disagreement from me on the magnitude of the polution problem, but I fail to see much leverage in his strategy. It's not as though the nuclear industry is, or ever has, missed a chance to claim its benefits relative to coal. There is the