Hundreds of documents released from DOE under a Freedom of Information Request and subsequent litigation shed new light onto DOE's management of an $8.33 billion loan guarantee on offer to support the construction of two new nuclear units at the Vogtle reactor in Georgia. The documents raise questions about how project risks were screened, the loan terms in the conditional committment agreement provided by DOE, the adequacy of the credit subsidy payments from borrowers to the US Treasury under the deal, and involvement by political appointees focused on getting the deal done.

The United States has more operating installed geothermal capacity than any other country, contributing nearly one-third of global capacity. Much of the market build-out is due to investments by the U.S. government and DOE in the late 1970s and 1980s, and more recently, to federal tax incentives (coupled with additional state and local programs, which are outside of the scope of this report).

Houston-based DKRW Advanced Fuels has a dream: they want to turn a chunk of Wyoming's vast coal reserves into 10,600 barrels of gasoline per day. They want to capture most of the carbon emitted in the process and sell it to the state's oil and gas industry, which will use the CO2 to inject into wells, increasing oil and gas production. In one fell swoop, the firm hopes to boost production of all of the state's major fossil fuels. The facility would be located near Medicine Bow, a town that presently has about 300 people.

Dreaming with somebody else's money

Oh, and part of the dream that they don't broadcast quite so loudly is that they want to do it mostly with our money. The firm has an application in with DOE for a $1.7 billion loan guarantee, which passed DOE preliminary review in 2009. And they've recently gotten approval from the Carbon County Commission to issue $245 million in tax exempt bonds. This debt is guaranteed by the project not by the County, but subsidized by taxpayers because the interest is free from taxation. It will also use up most of the state's annual alotment to issue tax exempt, non-municipal bonds.

There's more at the subsidy salad-bar: the Commission also unanimously endorsed issuing $300 million in industrial development bonds, which DKRW has asked the state's Permanent Mineral Trust Fund to purchase. From time-to-time, the Trust Fund does invest in Wyoming-based enterprises, and DKRW has indicated that they think their plant should be one of them.

The venture is also being supported by $10 million in state funding to support pre-construction studies both for the DKRW facility, and another project under consideration within WY that would convert natural gas into vehicle fuels.

Bob Kelly, executive chairman of DRKW, is happy so far with the state's involvement. As noted in a recent story in the Casper Star-Tribune, Kelly

said the bonds are "very helpful" in assembling the $1.7 billion to $2 billion needed to finance the plant's construction. Kelly said the company is seeking bank financing to cover the rest of the plant's cost [emphasis added].

Where's the equity?

Billions at risk, leveraged from other people. This should always be a flag that extreme due diligence is needed. The fact that the entire top management team at DKRW Advanced fuels (Robert Kelly, Jon Doyle, William Gathman, Jude Rolfe, Robert Moss, and Wade Cline) are out of Enron does nothing to ameliorate the concern.

Kelly's statement also begs the question "where's the equity"? DOE's guarantees require a minimum of 20% equity investment. It's not from DOE. It's not in the tax-exempt bonds, and it's not in the "bank financing to cover the rest of the plant's cost." That, perhaps, leaves the $300m that DKRW is trying to get the state of Wyoming to plow in. That funding seems to be structured like debt, because there is no mention of the state getting a stake in the company for the money. It is clearly like risk capital in terms of the investment it is supporting, however. Nonetheless, the limited equity requirement under the DOE program was focused on aligning the incentives of managers with the venture's success by requiring them to have "skin in the game." Government money wouldn't seem to cut it.

To it's credit, Wyoming is approaching the investment with some caution. The Treasurer's Office has requested input on deal soundness from the Wyoming Business Council, which in turn has asked for a technical review from Idaho National Laboratory. Mike Martin, at the Business Council, did not think the INL review went beyond technical issues to include as well a review of the financial suitability of the project for the state's Mineral Trust Fund. He was also not clear whether the INL review would examine systemic risk factors, such as what would happen to plant economics should a price or cap on carbon emissions be instituted. INL's review should look at both of these items, as federal and Wyoming taxpayers will have lots at risk if this plant moves forward with so much public subsidy.

A second check to the spending comes from the legislature. An investment of $300m would require Legislative approval, making it more difficult to put state funds at risk foolishly. However, investments up to $100 million would not, and State Senator Phil Nicholas, chairman of the Senate Appropriations Committee, has said the leadership would be comfortable with buying $50 to $100 million of the bonds. As evident from the table below, even at these lower levels, the funding would materially alter the Trust Fund's asset allocations and DKRW would comprise one of its largest, non-diversified investments.

DKRW investment conflicts with the purpose of the Permanent Mineral Trust Fund

To look at the issue of financial suitability, I pulled existing data on the state's Permanent Mineral Trust Fund (summarized in the table below). The purpose of this fund, and many others like it around the world, is simple: mandate a portion of mineral revenues to go into an investment fund for the benefit of future residents of the resource-producing region -- be it a county, a state, or an entire country. This solves two problems at once. First, the mandate removes from political control at least part of the massive cash flow that comes from resource booms. Without such a mandate, the potential benefits of resource booms were often lost as politicians squandered the surge in funds on foolish projects, empire building, or corruption. Second, the Trust Fund approach requires an independent fund manager to invest in a widely diversified set of assets. The income and growth of these other assets reduce the correlation between energy or mineral prices and the available revenues to the state, helping to dampen the boom-bust resource cycles as well.

Based on the criteria for which the Mineral Trust Fund was established, investing in DKRW should be immediately rejected, even at funding levels well below the requested $300m. Regardless of whether INL decides the plant is technically sound, the investment further concentrates Wyoming's financial exposure to energy prices rather than diversifying away from them, and therefore works counter to the intent of the Mineral Trust Fund.

Further, as shown below, the scale of investment is far more concentrated that what currently exists in the Fund's portfolio. At first blush, a $300m investment in the plant may not seem like a big deal, comprising well less than 10% of more than $5 billion in total holdings of the Trust Fund. Yet, for any of the conceivable asset classes in which the investment could fit, exposure to DKRW would dominate the class, comprising at least than 2/3 of the resultant asset class sizing (current size plus DKRW holding) in every case. This metric actually understates the risk since the existing portfolio has many small investments, rather than large lumpy ones like the proposed holding in DKRW.

I looked at four potential asset categories in which DKRW could possibly fit. Because the investment would be debt with no equity interest, I considered corporate bonds. However, the risk of this venture is far higher than what a normal corporate bond portfolio would entail; and if I were the Treasurer, I would require equity interests as well. If we assume the state were to get an equity interest as well, conceivably small- to mid-sized (SMID) US equity would be an asset-class fit. But again, the risk is higher than what a SMID portfolio would normally entail due to the high technology risks of the plant, and the investment would have some elements of debt rather than being pure equity. Private equity is probably the best match in terms of risk level -- though one that would require much higher returns to the state than what is likely being considered at present.

The final category considered was intra-Wyoming investments. Like the other possible categories, DKRW would come to dominate the WY holdings at a $300m sizing. Not only would be the size of the investment be larger than what currently exists within the intra-WY holdings, but many of the existing investments benefit multiple firms or people, not a single project. Many of these projects also have a clear public interest component (beyond simple job creation), something that DKRW investment does not.

For additional reading on the planned DKRW coal-to-gasoline plant in Medicine Bow, Wyoming Public Radio just did an interesting series of reports. Taxpayers for Common Sense also has a good backgrounder. Update, 2/16: An interesting op-ed in the Casper Tribune by Jason Lillegraven goes into some detail on problems with the environmental assessments done on the project to date, particularly with regards to water consumption. For so many of these facilities, water is the achilles heel. Too often, the facilities pay little or nothing for the amount of water they use. Just as running a sensitivity on project returns assuming CO2 emissions won't always be free, it would be prudent to do the same with water.

Wyoming Ownership of DKRW bonds

I. DKRW wants fund set up to diversify away from minerals to invest in CTL

Fund that would own the bonds

WY Permanent Mineral Trust Fund

State investment requested by DKRW

$300,000,000

Total Fund holdings, 6/30/11

$5,050,000,000

II. Concentrated DKRW investment would dominate any asset class it is attributed to

Possible asset class categories for DKRW investment

Asset class holdings as of 6/30/11

DKRW investment/ existing asset class sizing

Corporate bonds

$189,100,000

159%

Small/mid cap US equities

$186,200,000

161%

Private equity

$129,500,000

232%

Wyoming investments

$121,300,000

247%

III. Scale of DKRW investment would be much larger than other intra-WY investments

Amount Outstanding, 6/30/11

DKRW Investment/ Existing WY investment

Largest WY Investments

Time deposit open banking program (multiple beneficiaries)

$162,100,000

185%

Basin Electric Power Bond

$33,702,000

890%

Farm loans (multiple beneficiaries)

$28,851,596

1040%

Shoshone Municipal Pipeline Treatment Plant

$13,286,088

2258%

Laramie Territorial Park Loan

$10,000,000

3000%

Source: Wyoming State Treasurer's Investment Report, Fiscal Year 2011, September 2011

As fallout from the Solyndra bankruptcy continued to build, Jonathan Silver, Executive Director at DOE's Office of Loan Programs finally stepped down. This outcome couldn't have been a total surprise for him: Silver came from a venture capital background, knew the failure rates of DOE's projects would likely be high, and understood that the bets DOE was making were orders of magnitude larger than what had been done before. In an interview with Politico earlier in the year, Silver noted that the scale of credit supports his office was providing were massive. “These are the biggest transactions in our industry," he said. "No one is working at a scale like this — anywhere.” Maybe even DOE will stop now.

Silver is leaving DOE to become a distinguished visiting fellow at DC policy shop Third Way. Having played many years ago as a (not very good irregular) on Rep. Chet Atkin's (D-Mass.) softball team, led at the time by Third Way founder Jim Kessler, I've no doubt that Third Way will be a fun place to work. In terms of energy policy though, I'm expecting more "Washington Way" than "Third Way" from Silver there: a continued focus on large scale government subsidies to favored energy sources.

This philosophy seems to be much in line with Third Way's own thinking on these issues, at least in regards to nuclear. In a January 2010 policy piece on nuclear financing Third Way advocated for "at least $100 billion" in loan guarantees to nuclear (p. 1), a figure in line with the most extreme industry boosters such as NEI. The paper further noted that even this wouldn't be enough, and that other types of supports would also be needed. A paper later that year on small reactors again advocated for large amounts of earmarked government subsidies to nail down designs and build the first set of reactors. As soon as you do that, they argued, prices would fall with experience and reduced perceptions of risk. Yet the fact that these exact same arguments have been made by the nuclear industry since the mid-1950s, and the reactors are still uncompetitive without very large subsidies, did not seem to carry much weight.

Back in April of 2010, I was researching nuclear subsidies in depth for this report, and Third Way's presentation of nuclear finance as a critical path item for clean energy seemed off to me. I sent the authors a series of questions to help clarify their position on the high risk and costly recommendations they were making:

1) It seems as though your support for larger loan guarantees for nuclear is predicated on the grounds that nuclear power is needed to address climate change. If it could be shown that other mechanisms of pulling carbon out of the economy were less expensive, faster, and lower risk, would your support for large credit subsidies to nuclear change? Would you favor competitive tendering of subsidies to carbon-reducing energy technologies in order to minimize the public cost per mt of CO2e avoided over earmarked subsidies to specific forms of energy?

2) The US economy quite regularly develops innovative risk syndication approaches to bring high risk/high reward ideas to fruition. Venture capital, for example, brings millions of dollars into enterprises with no existing assets. In evaluating the argument that low market cap for utilities precludes the ability to privately finance nuclear plants, did you explore the variety of alternative risk sharing mechanisms -- from joint ventures and power purchase agreements -- that could have overcome the market cap constraint?

3) Your paper repeatedly states a need to bring financing costs down for the nuclear sector. Does this reflect a belief that these capital costs are not reflective of real market risks, and therefore unimportant to reflect in delivered power prices? I would argue that far from shifting these risks on to taxpayers, you want to be able to differentiate high capital risk power sources from low ones; and that removing this differentiation creates large barriers to entry for smaller scale, more rapidly deployable technologies.

The large nuclear projects require third party credit assessments of the project absent the loan guarantees. Would Third Way support making those documents public to the parties (i.e., taxpayers) taking on the credit risk?

4) You advocate CEDA [Clean Energy Deployment Administration] as the best path forward. Has Third Way done any formal review of institutional checks and balances in the CEDA proposals, and assessed the incentive alignment of key decision makers? If so, could you please send it to me? My reviews of these issues have found the schemes quite wanting and at high risk of failure.

As an aside, your mention of CBO's scoring of the nuclear loan guarantee program at only 1% seems inaccurate. One nuclear-specific review of nuclear economics scored the subsidies via loan guarantees at zero, under the assumption that the credit subsidy would fully prepay the default risk. That author has acknowledged to me that this represents an assumption rather than a certainty. Later CBO reviews did assume a 1% net interest rate subsidy (after credit default payments), but did so as a place holder because they were concerned DOE would try to represent the guarantees as zero cost. CBO has not done any type of scenario modeling of this, due to a requirement on them to produce point estimates. However, in conversations I've had with some of the staff they do recognize that losses could be far higher. In fact, a 2003 review by CBO of nuclear loan guarantees surmised a 50% default rate and about 25% net loss after post-default recoveries.

5) Do you have any examples in which the federal government has successfully selected and monitored highly concentrated credit support (on the order of $5-8 billion for a single investment) for private investment? I'd very much appreciate if you could send me the example, as I've not yet found one. Note that bailouts to large, diversified firms such as AIG or Goldman Sachs would not meet this criteria because (a) they were initiated for very different reasons; and (b) they are supporting a wide range of activities not a single industrial facility. Furthermore, these and other historical bailouts normally give the taxpayer stock warrants to compensate to some degree for the risk taking. To my knowledge, these are not being considered in any of the lending programs.

Initially, I got no reply. A follow-up query ten days later did generate a fairly perfunctory response from report author Josh Freed. He noted that the paper "stands on its own," and suggested that I look at their website (he sent their main url, not links to specific pages) to find their thinking on nuclear and clean energy issues. He did not respond to a single specific question.

Note that in August 2011, Wendy Kiska and Deborah Lucas at CBO did a much more detailed look into subsidies associated with nuclear loan guarantees (see item 4 above), and found that the subsidies were substantially higher than the 1% placeholder value that Third Way referenced. A half-billion dollar default on the Solyndra loan guarantee, use of subsidized credit to export jobs by electric car company Fisker, and the massive damages (and systemic cost increases to nuclear reactors around the world) from the Fukushima accident have all underscored that the loan guarantees Silver and Third Way have been advocating we distribute like candy really are high risk, expensive instruments for which funds are often deployed in ways different than what the policy wonks initially envisioned. It is a lesson worth remembering.

1) Don't Prop up USEC. Henry Sokolski of the Nonproliferation Policy Education Center and Autumn Hanna at Taxpayers for Common Sense weigh in at the National Review Online on a proposed $2 billion dollar loan guarantee to finance new enrichment facilities for the United States Enrichment Corporation (USEC). USEC is the privatized residual of the government-run Uranium Enrichment Enterprise that ushered in the US nuclear era. In Another Solyndra: Ohio Republicans join the energy-subsidy racket, they argue that politics are leading the push of put taxpayer money at risk despite an extremely poor business case.

The business case should matter far more than it seems to in Washington. And this is so not just for each specific subsidy recipient, but also for how, in the aggregate, these interventions distort price signals and market structure overall.

With so much focus on solar subsidies, it is useful to point out that even if USEC doesn't get the guarantee in the end, they've already scored up to $300 million in federal money to "help USEC reduce the technical problems that forced DOE to reject USEC’s original application" for a Title 17 loan guarantee. That's bigger than the face value of many of the loan guarantees granted to renewable borrowers.

2) Anybody got a light? The effort to get the blaring light of fiscal conservative oversight now shining on Solyndra directed at least a tad towards the Vogtle nuclear deal proceeds on the dual tracks of litigation and legislation. Legal action by the Southern Alliance for Clean Energy (SACE) and Taxpayers for Common Sense to expose the terms of the loans continues, as DOE produced only heavily redacted documents in response the last FOIA request.

Of particular interest to SACE is information revealing whether company officials played an inappropriate role in shaping the terms of the loan guarantee. Based on the limited information produced, it appears that the power companies had to put almost no skin in the game, promising to pay a credit subsidy fee of possibly as little as 0.5 or 1.5 percent of the total loan guarantee.

House Democrats have been pushing for greater oversight legislatively as well, with a letter drafted by Rep. Henry Waxman (D-Calif.) and co-signed by Reps. Ed Markey (D-Mass.) and Diana DeGette (D-Colo.) to Chairmen Fred Upton (R-Mich.) and Cliff Stearns (R-Fla) of the House Energy and Commerce Committee. The letter notes that while they support a broadening of the Solyndra review to include 27 loan guarantees for renewable energy (something that has already been implemented), $10 billion in conditional guarantees to nuclear projects should also be included. This follows up on a similar push by letter co-signer Ed Markey last month.

In my book, this one is simple: if you aren't willing to look at potential conflicts of interest and corruption in all of the projects, don't call yourself a fiscal conservative.

3) Cash is cash, or don't cry when we invest your money abroad.Fisker Motors, recipient of a $529 million loan from the US DOE, is doing what any corporation does: it tries to find capital at the lowest possible cost and deploy that money however it sees fit to meet its own internal objectives. In this case, that means putting funds into manufacturing jobs abroad (or, per the input from Media Matters below, using the funding domestically to free up other funds to finance foreign manufacturing jobs). Oops.

On the other hand, as a major debtor to the firm, wouldn't taxpayers want Fisker to increase their chance of success as much as possible? Or, if you want to see electric vehicles enter the marketplace, wouldn't you want to maximize operational flexibility as well? I suppose that's the problem with having multiple objectives (is the loan for making jobs in the US or for trying to develop a new energy technology?).

Media Matters points out that the overseas construction was known prior to the loan guarantee being approved, implying this controversy is merely a manufactured issue. I disagree. The example underscores the core point that promoters of big federal subsidies too often ignore: in a global economy, building an industry from scratch doesn't mean it will all (or even mostly) be built here.

4) Risk is risk, or don't cry when bankruptcy or dilution come to call. The time for pricing risk is before you provide the credit. Happy talk about guarantees not really being subsidies (yes, we're talking about you, Dick Myers) should always be ignored by taxpayers and Congressmen alike.

A. The Belly-Up Club: Beacon Power becomes member number two. Flywheel producer (for bulk power storage) went belly-up today. Taxpayers were on the hook for $43 million. This, and Solyndra, will be good tests for the claims put forth by program promoters in years past that recoveries in bankruptcy will be substantial. Let's hope so.

Recoveries aside, expect more members in the Belly-Up Club soon. If we take the loan guarantee program to be what it really is -- investments with risks similar to venture capital or start-ups, expect failure rates of around 30-40%. If you expand the outcomes to include failure plus no return, we're up to 70-80% of the pool, according to Harvard Business School senior lecturer Shikhar Ghosh. Since Ghosh is talking private firms, and the incentive alignment within the Title 17 program between managers and the long-term performance of the firm is much worse, I'm expecting loss rates within the funded portfolio to be even larger absent big changes in the market (e.g., implementation of a large carbon tax).

B. Diluting the feds. Andrew Stiles raises concerns at the National Review Online that the restructuring of financing for Solyndra prior to its bankruptcy, a process that subordinated the Treasury's position in any subsequent bankruptcy, was illegal. He links to a series of e-mail chains on the restructuring, which are quite interesting in their own right:

Discussion of subordination starts on PDF page 14.

Page 21 notes that since July 2010 DOE was refusing to provide information on the Solyndra loan guarantee even to Treasury (which, of course, was backing the financing). This type of behavior underscores the concerns I had with program transparency and accountability back in 2007.

Page 22 indicates that Lazard was the firm providing independent review to DOE, perhaps of the original deal or perhaps only for strategic options for Solyndra at that point in time. There has been very little visibility on who the financial advisors to DOE have been on the Title 17 program, and therefore on the real or potential conflicts of interest these advisors may have. This is a problem.

Page 29 raises the intriguing possibility that investors may have been interested in keeping Solyndra alive longer to allow them to strip more assets from the firm (thereby reducing the government's collateral). Artificially high discounting of accounts receivable was one area mentioned.

While the lawyers will toil back and forth on the legality of subordination under the Title 17 authorizing legislation, to a great degree (and assuming there was no fraud or gross negligence within the government in the restructuring) it seems besides the point. If the government wants to do high risk investments, those investments go bad with surprising regularity. Any new money won't go in at the old terms. Either accept the risk of dilution, or don't play in the market.

Defenders of Title 17 energy loan guarantee programs periodically point to the many other areas of the economy in which the government makes direct loans or guarantees. They use the other programs as evidence for two main points: that the government is experienced and skilled in leveraging public credit to support private activities; and that what is being attempted in the energy sector is no different from what lots of other industries already get. A recent commentary by Mark Muro and Jonathan Rothwell on the Brookings Institution web site makes this argument, pointing out that

The U.S. government runs some 70 loan guarantee programs and 63 lending programs that catalyze the financing of everything from transportation infrastructure and rural housing to science parks. More than $3 trillion of taxpayer money is at risk in these programs...

It is true that like all of these other programs, the energy credit support boosts the available financing for targeted projects. However, Title 17 is by no means comparable to a college loan, farm mortgage, or even the majority of export credits.

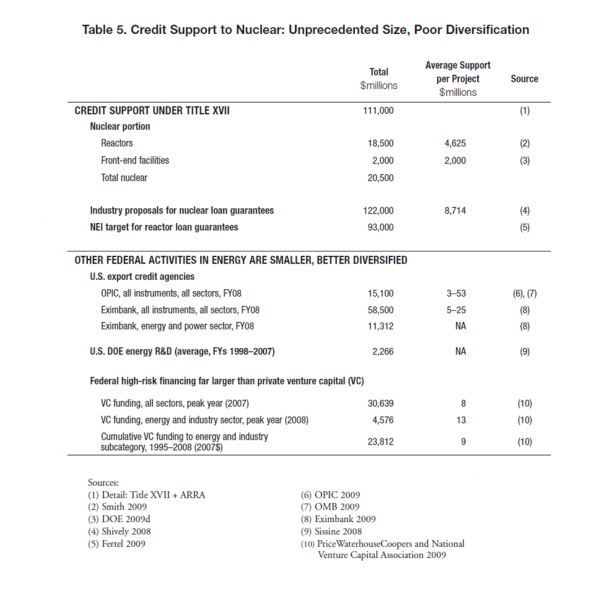

Scale. The Solyndra guarantee was for more than $500 million; most of the DOE guarantees are in the hundred million dollar range or above. Those for nuclear power range from $2 to $8 billion in credit exposure for a single project. This is dramatically different from other programs. Average credit supports for OPIC and Eximbank, for example, are generally well below $50 million per project. Average venture capital investments in the energy sector were also much smaller, generally less than $10 million per round. Table 5 (below), excerpted from a detailed review I did of subsidies to nuclear power earlier this year, provides more resolution comparative scales.

Technology risk. All federal lending programs face some risks of default, due to changing markets or economic conditions of the borrower. However, the energy credit programs also face a tremendous amount of technology risk. The instruments are priced as though they were run-of-the-mill projects being financed. In reality, however, the unproven technologies make them more akin to venture capital than to a standard project finance loan.

Concentration of risk. As the scale of credit risk for individual deals rises, the impact of single defaults on the overall portfolio performance become increasingly important. Title 17 offers far less ability to use a mixed portfolio of commitments (e.g., a diversified mix of geographic locations or industry types) to offset the risks associated with single loans than exists for other programs (OPIC for example) that have a larger number of smaller scale, more diversified lending commitments. Furthermore, many of the supported projects face large systemic risks from events beyond their control. Chinese subsidies to solar put at risk many of the supported solar projects. Natural gas fracking (driving power prices down) and the Fukushima accident (driving nuclear power prices up) put at risk the ability for any of the proposed nuclear projects to be competitive.

Poor transparency. Very little is known about the terms of the deals being struck, how loan guarantee "winners" are being selected by the small number of people involved in decision making, and potential conflicts of interest. How closely do the number of actual jobs created by a guaranee match the job creation claims on the application? On what basis was the credit subsidy on the loan calculated? Does the federal government have an equity participation should the high-risk investment pay off? Do any of the specialists involved in vetting the loan guarantees or the credit risk have conflicts that would bias their input? Surely there are ways to make much more information known to the public without revealing confidential business information. The Solyndra bankruptcy will hopefully lead us in that direction.

Finally, Muro and Rothwell suggest that despite the bankruptcy, there is a possibility that the taxpayer will be made whole. They underscore this point by reporting an asset value for the firm that exceeds the loan guarantee amount. Yes, the feds may get something. But we need to be realistic here: if liabilities didn't exceed assets, the firm wouldn't have declared bankruptcy. This means that the total debts of the firm go well beyond the federal loan guarantee that is attracting so much attention; and that the federal government is not the only creditor. Taxpayers will share in whatever is left on an equal basis (pari passu) with other creditors of a similar rank in the bankruptcy; original proposals to give DOE first access to assets in a bankruptcy were eliminated as the proposed rules for the program went final. Further, pre-bankruptcy asset values are often steeply discounted once the firm ceases to be a going concern, likely reducing recoveries still further.

Source: Doug Koplow, Earth Track, Inc. Nuclear Power: Still Not Viable Without Subsidies, (Washington, DC: Union of Concerned Scientists), 2011.

Congressman Ed Markey (D-MA) sent an interesting letter to Fred Upton (R-MI) late last week. The correspondence outlined some of the history of the Title 17 loan guarantee program and the nuclear industry's push to make it their own. It also included examples of the role the Nuclear Energy Institute played to weaken federal recourse in a loan default, and the pressure it brought to bear to expedite loans to its members. These are indeed crass examples of political lobbying that put billions (and potentially tens of billions) of dollars of taxapayer money at risk.

However, the most troubling element of this event to me was the political intervention with OMB's traditional role in financial oversight of federal programs by then-Senator Pete Dominici. This is from Markey's letter:

Additionally, at the July 26, 2007 Senate Budget Committee hearing on the nomination of Congressman Jim Nussle to be the Director of the White House Office of Management and Budget (OMB), then-Senator Peter Domenici raised the pace and problems associated with DOE's implementation of the loan guarantee program:

"But OMB has been dragging their feet and I do not know which cabinet members have been involved. I surmise as of now the Secretary of Treasury is himself involved. But I can tell you, Mr. Nussle, that this is one of the most important provisions of the Energy Act. It should have already been done and it should have had $25 billion to $30 billion in the loan guarantee fund. It is still not ready and the recommended amount by OMB is $9 billion. That will not fly...It seems to me all the work that has been done, you have got about 48 hours, to sit down and get this fixed."

On August 2, 2007, Senator Domenici lifted his hold on Mr. Nussle's nomination and voted to confirm him after receiving "a commitment from the Office of Management and Budget to fulfill the vision of Congress with regard to the Department of Energy loan guarantee program."

As I noted in my earlier blog post on Solyndra, this default is not just about subsidies to one industry or another. It is about what role governments should play in the marketplace; and whether we are able to set up governmental structures that align the incentives of parties properly, and that both establish and retain appropriate checks and balances to reduce the risk of corruption and taxpayer loss.

Domenici has always felt passionate about nuclear power in this country. Yet even if we grant him that his promotion of nuclear has been rooted only in his belief of what was good for the country, his actions are inexcusable. Undermining the program structure for something he likes creates flaws that quickly spread more widely to all sorts of programs, bleeding the country in the process. Will the appointment of competent fiscal management for OMB now rest upon the whims of key Congressional members pushing for OMB to reinterpret financial reviews in their favor? What other tests for how many other positions will crop up in its wake? Parochial interests can very quickly corrode the basic structures we need to govern effectively if they are allowed to run unchecked.

In the Solyndra bankruptcy, Congressman Upton has been given an opportunity to put the loan guarantee program overall under scrutiny that was not possible back in 2007. There are records of decisions, a number of commitments, and a broader context of financial failure and recession against which to judge the initiative. Because I know the Congressman cares about the country, he would do us all a service to ensure his review looks not only at Solyndra, but at the way the other deals were struck as well. That includes the the $10.3 billion in nuclear deals that Congressman Markey has asked be reviewed, and of course the next largest single commitment as well -- $5.9 billion to Ford Motor Company.

Under the terms of Title 17, many of the borrowers must pay advance funds to cover their "credit subsidy." This has been roughly estimated as the probability of default times the net losses to the feds (after any recoveries in bankruptcy) should one occur. The industry has consistently pushed for lower credit subsidies, arguing that not only did their deal have a low risk of default, but even if it did default, taxpayer recoveries in bankruptcy would be high. The Solyndra bankruptcy provides a real-world case study to put test these claims. Congressman Upton's review of Solyndra should look very carefully at how high those recovery rates really are. Will they be 50% of the investment? 25%? Close to zero? This will provide quite important information by which we can judge credit subsidy estimates in any future deals.

"The six financial institutions below (Citigroup, Credit Suisse, Goldman Sachs, Lehman Brothers, Merrill Lynch and Morgan Stanley) are convinced that loan guarantees are an important tool, along with supportive state government policies, to enable the financing in the credit markets of new nuclear power plants in the United States. We are concerned that the Proposed Rule is not workable, and are providing our perspective in the hope that it will assist the Department of Energy in developing final regulations to implement this essential program.

Those of us who have been railing on the government's increasing push to make massive loan guarantees available to individual energy firms are not surprised to see the first major bankruptcy. Solyndra went down with $535 million in federal guarantees for lots of reasons. The marketplace is increasingly competitive. Power prices have fallen due to recession and fracking-induced reductions in the cost of natural gas. China subsidizes its solar production, artificially manipulates exchange rates, and there is a growing supply overhang as PV subsidies in Europe get cut. New technologies look to be better than Solyndra's. John Hudson in The Atlantic's blog provides a nice overview of the political hemming and hawing as the parties try to frame the issue to protect their interests.

Though all of these reasons are plausible contributors to the demise of Solyndra, they are hardly surprise risks. Operational problems, competitors, changes in market conditions: all are baseline risks for any type of new investment that a venture capital firm might take on.

The difference isn't the nature of the risks, but rather the nature of the investor -- the federal government, straying far from its domain of demonstrated competance. This is the core issue I see in the Solyndra situation, but one that seems to be getting overlooked. The Title 17 loan guarantee program, in all of its various forms including a swath of more recent even larger plans to have a federal "Clean Energy Bank", is poorly structured to achieve success. It puts a handful of largely invisible bureaucrats and advisors in the position of making unprecedented wealth transfers to fund high risk private ventures. That last sentence alone should have been enough to doom the program by both the Bush administration (that passed it) and the Obama administration (which has been approving most of the lending commitments).

Yet there are other program weaknesses as well, compounding the barriers to success. The risk assessments are not subject to much disclosure or vetting on the outside, and the payments from funding recipients (in the form of credit subsidy assessments on borrowers) are widely recognized to be well below the market value of the credit guarantees. Thus, the riskier the venture, the better the federal guarantees look to the firm, dramatically increasing the adverse selection risks of the resulting portfolio. Yes, I know -- there is government review of the deals to alleviate those risks. But this is done by people with only their goodwill to rest upon; they have no personal financial risk bound up with making a good selection, may not always have the appropriate technical expertise, and have limited time. And because the financial benefits from getting one of these loans are so high, the government review team is arrayed against the best talent money can buy. There may be conflicts of interest as well; it is really quite hard for the public to know at this point as many of the key decision makers and reviewers are not named.

The structure of this program has many red flags indicating a high risk of failure and corruption. Other than scoring political points, it hardly matters that a solar firm is the first one to go down. The Vogtle nuclear reactor loan guarantee is roughly 16x larger, and was done at terms based on market structure prior to Fukushima. Anybody want to bet on the default risks for that one as the operating requirements for reactors get ratcheted up in response, and natural gas plants continue to undercut everybody's pricing?

Back in 2007 DOE was taking comments on their notice or proposed rulemaking (NOPR) for Title 17. I put in a number of comments on program structure, which, as far as I can tell, were entirely ignored by DOE. The Department focused instead on the comments from the big investment banks that would be financing these deals. Lehman Brothers and Merrill Lynch, neither of which exist any longer, comprised a two of the six financial institutions that banded together to submit joint comments on how the multi-billion dollar loan guarantees ought to be structured to work for the banks. Citi, Goldman Sachs, and Morgan Stanley, all of which went through dramatic restructuring and public bailouts, made up most of the rest. Their comments resulted in even more generous terms for borrowers, and weakened checks and balances for taxpayers. Below are some excerpts from the comments I submitted.

The NOPR did not go far enough in outlining how DOE would ensure non-political allocation of resources and protection of taxpayer capital. Many of the ways these issues were addressed in the current version were mostly descriptive in nature, leaving too much guesswork about how actual implementation and institutional oversight will proceed.

...

A combination of wide latitude in determining project eligibility to participate in funding rounds with imprecision on how performance "improvement" will be measured create the conditions for skewed and politicized distribution of billions of dollars in guarantees. These conditions bode poorly for the long-term success of this program.

...

DOE acknowledges wide latitude in targeting loan guarantees and acknowledges they are under no obligation to run open contests across all energy sources authorized under Title XVII of the Energy Policy Act. The NOPR is mostly silent on the establishment of rigorous project comparison metrics and robust institutions that would ensure the billions in guarantees are effectively targeted.

Not all energy resources eligible under the Energy Policy Act of 2005 (EPACT) are necessarily eligible in particular -- or indeed any -- funding rounds. In fact, DOE's NOPR lists specific programmatic objectives, loan guarantee authority or available funds as possible criteria by which guarantees under Title XVII can be awarded. The NOPR includes the example (p.7) of the Administration's 2008 budget that proposes $4 billion in guarantees for centralized power, $4 billion for biofuels and other clean fuels, and $1 billion for new electric transmission or renewable energy power systems. This example is an early indication of the power that the legislative or executive branches will seek to exert in earmarking funding to favored interest groups. The political influence leveraged by these groups is greatly enhanced by DOE's view that Congressional appropriations are needed to support DOE's credit authority under Title XVII, and that Congress can structure these appropriations however it sees fit. While in theory the executive and legislative branches could choose to exert their influence based on the technical merit of the projects alone, assuming they will in fact do so would be both imprudent and naïve.

The risks of political influence are further compounded by the fact that funding under Title XVII will be in the form of loan guarantees, for which valuation and transparency are far more difficult to attain than with direct payments. In addition, recent mandates to publish legislative earmarks (albeit only partially effective thus far even for direct payments) would not seem to apply at all to Title XVII loan guarantee decisions.

By the time the larger lending proposals under CEDA started to surface in 2009, I was a bit more blunt in my concerns about corruption:

CEDA risk profile likely to be far more concentrated than conventional banks, increasing potential problems with systemic risks and corruption. The multi-billion dollar scale of centralized energy technologies suggest the size of the credit commitments for individual projects under CEDA will be far larger than undertaken in other areas of federal credit guarantees. This opens the initiative to higher systemic risks and potential corruption.

It will be interesting to see what surfaces in the FBI review of documents. It's a pity we can't learn about potential political influence on the nuclear deals at the same time, but Congressional sources tell me it is not about to happen. At least the Solyndra failure can serve as a wake-up call on the incentive problems for these mega-lending initiatives, and help us avoid far worse financial blow-ups were we to have followed industry's lead in ramping up lending to nuclear or establishing a large scale "green energy bank" such as CEDA.

UPDATE, September 19th. Michael Grunwald at Time Magazine has a nice overview of the problems with shining a light only into a small part of a big swamp. Focusing on Louisana Senator David Vitter, Grunwald documents how Vitter's bill to increase scrutiny only of loan guarantees to renewable energy projects side-steps Vitter's own efforts to bring home the loan guarantee pork to his own constituents -- including for renewable energy projects. We've got systemic problems here, and piece-meal solutions generally just shift the problem rather than solve it.

Ben Gemen over at The Hill describes as "hardball" the effort by House Republicans to bring to light documents and decision making behind a $535 million loan guarantee for a new facility to be built by Solyndra. Hardball is appropriate for an unprecedented level of taxpayer exposure for investment into individual, privately-owned assets.

I hope the Congressional effort is successful in teasing out real documents that would allow real oversight of DOE's loan guarantee program. DOE's Loan Programs Office has been notoriously resistant to transparency, despite operating at a scale that already runs into the tens of billions of dollars of commitments ($39.8 billion as of July 2011). Proposals to extend this federal-financing approach through a "clean energy" bank of sorts have been floated with figures in the hundreds of billions. This is not a program to be glossed over.

Gemen reports that

In a letter to [Rep. Cliff] Stearns Tuesday, OMB Deputy General Counsel William Richardson, Jr. notes that OMB "made available" 1,400 pages of emails and attachments this week, which follows hundreds of other pages made available earlier.

It is impossible from the outside to tell how material this information is, and whether the critical items on risk management, potential conflicts of interest, and likelihood of market success have been provided.

Nonetheless, I'm guessing that the data dump on Solyndra is about 1,400 pages more than what has been provided for DOE's commitment to the Vogtle nuclear power project in Georgia. At roughly $8.3 billion (which is really a direct loan, as program rules require a loan of this scale come from the Federal Financing Bank), DOE's support for Vogtle is nearly 16 times as large as what taxpayers are risking for Solyndra. Surely if a subpoena is warranted for gathering data on the Solyndra project, it is warranted for Vogtle as well.

I have been critical of the weak structure of DOE's foray into large scale loan guarantees for energy infrastructure since the program's inception. It is not as though the Department has a robust and successful history of this type of capital deployment. Here are the my formal comments to DOE on the proposed program structure back in 2007. They were ignored then; DOE focused mostly on loosening program rules during that round of comments based on input from interested investment banks, firms that did or would represent many of the beneficiaries of the guarantee program itself. Some of these banks (e.g., Merrill and Lehman) imploded soon after due to the very types of conflicts of interest and weak oversight that remain a concern in the DOE lending initiative.

Though DOE remains under pressure to push money out the door, and in the process continues to ignore most of these structural issues today, the problems -- and the financial exposure -- remain. It would be a service to all taxpayers if Cliff Stearns extended his interest in fiscal prudence and oversight beyond a single project and to the program overall.