When the drinks are flowing at the open bar, it's not a big surprise that patrons swarm for their free pints. Tax bills are the same, with amendments aplenty as the hours ticked on towards the Senate passage of a massive tax reform package last week. Hey, when you are spending somebody else's money and nobody has time to read what you are sticking in anyway, why not take a gander on a nice payout for your district friends?

Here's a rundown of a few energy-related items of interest in the tax bill. The Senate version, with hand markups and all, and run through OCR so you can search it, can be accessed here.

1) Wildlife reserves are for drilling

Tax bills aren't just for taxes, and wildlife reserves aren't just for wildlife. After decades of trying, the Senate moved to open the coastal areas of the Alaska National Wildlife Refuge (ANWR) for oil and gas exploration and leasing (see Title II, page 474) of the bill.

Some background on the remaining hurdles and not so great economics of oil and gas in ANWR are found in this useful piece by Oil Change's Andy Rowell. Analysis I did with the Stockholm Environmental Institute looking at field-level data across the US also indicated these areas well below breakeven at current market prices.

No such ambiguity about the move can be seen from Alaska Senator Lisa Murkowski though. She fought hard for this change and believes it'll bring great wealth even if scientists and economists don't. But other short-term factors are also driving this decision. First, Alaska's budget remains heavily dependent on oil and gas revenues -- something that aging fields and falling prices have hurt. Second, the Trans-Alaska Pipeline System (TAPS) needs more product to keep the unit costs low and the infrastructure maintained. Indeed, it turns out that getting flow from ANWR was a core assumption when it was designed.1 And boosting the flows will reduce unit costs, reduce operating costs (low flows in a massive diameter line cost more to keep moving), and boost confidence in continued service to existing fields that would be stranded were the line to close. One final benefit of keeping TAPS running: pipeline operator Alyeska can continue to defer its responsibility (and associated cost) to dismantle the pipeline and clean up the right-of-way.

Oil revenues are easier to measure than fish and wildlife values, and there is quite a bit of wildlife in the areas being opened for drilling. Audubon magazine notes the region being opened has the highest biological diversity for any protected area above the Arctic Circle.

Look for low realized values on the lease sales due to a low price environment, remote and expensive fields, and a high risk of delays from court challenges. Expect state or federal subsidies to infrastructure, perhaps combined with weak financial assurance requirements for the drillers to spur deals along. And finally, expect some spills and other damage to natural resources. All will erode the net gains to the state from this move.

But in the arcane rule of budgets, all that counts is the gross gain to Treasury from the sale of a natural resource, resulting in net offsetting receipts of $1.1 billion according to CBO. Not much in the context of an increased deficit of $1.5 trillion, and even this low value treats as zero the damages to natural resources or other property values. But that, unfortunately, is how this rather bizarre world operates.

2) Strategic reserves are for selling (to help offset continued subsidies to hedge fund managers)

The very last section (Section 20003) of the Senate bill authorizes the sale of $600 million of oil from the Strategic Petroleum Reserve in 2026 and 2027. This is a very small amount of money at the very end of the scoring period for this bill. Yet, it does help a bit to offset some of new tax subsidies in the bill.

How's it relate to hedge fund managers? Because the Senate instituted a 3 year holding period (up from one) on private equity and hedge fund carried interests, boosting revenue by only $1.2 billion over 10 years. Had they instead eliminated carried interest subsidies altogether, tax revenues would have been increased by $16 to $180 billion over the same period.

Not making the hard decisions leaves the Republican Senators using a combination of gimmicks, like selling oil from SPR starting in 9 years -- and simply running up the debt -- instead.

3) Tax-favored status on pass-throughs confirmed to apply to MLPs

Pass-through entities escape corporate level taxation, but historically were taxed at the individual level based on the economic situation of the individual partner. Many of these partners are wealthy and taxed at the highest marginal rates. They don't like this.

The House bill caps the individual rate on income from pass-throughs at 25%. The Senate bill instead allows up to 23% of expenses to be deducted from taxable income, with a similar effect on the effective tax rate. Earlier versions of the Senate bill capped deductions at 17.5%; boosting it to 23% increased the revenue loss by $114 billion (to a total of $476 billion) over the 2018-27 period.2

A last-minute amendment sought to expand this benefit to both MLPs and to financial PTPs such as Blackstone. Only the first got through -- though it's a big one. It further extends the tax subsidies on offer to oil and gas MLPs by reducing the taxes even the partners have to pay.

I remain unclear as to whether even the financial MLPs are fully frozen out of this new subsidy. To the extent their energy investments are organized as limited partnerships within the larger PTP, income would flow out of the investments both to the parent company (and those invested in the traded shares) and directly to the limited partners who have bought into the individual investments or investment funds. For this latter group, my assumption would be that the lower tax rate would apply. Please email if you know the definitive answer on this.

4) LIFO no more for Grandaddy; but still available for ExxonMobil

Any tax rules that enable taxpayers to deduct a higher proportion of their expenses more quickly generates a financial benefit on a time-value-of-money basis. Inventory turns out to be important in this way. Firms usually have many identical products in their inventory -- whether barrels of oil or computers. When they sell a product, they deduct the cost of that product (via cost of goods sold) from revenues in order to calculate the taxable income. The costs of that product are not identical over time: commodities may change sharply in value over the inventory turnover cycle; and during periods of inflation costs across all sectors can change quickly. The freedom to deduct the highest COGs sooner can greatly reduce near-term taxable income.

Historically, firms could choose whether to deduct the costs of each sale based on the COGS for the oldest item (or barrel of oil) still in inventory (FIFO, or "first-in, first-out"); or select more recent costs if those were higher (LIFO, or "last-in, last-out"). This same logic applied to people's stock portfolios. It Grandad bought 400 shares of Apple Computer for $10 share (split-adjusted) back in 2006, and another 400 shares at $115 each back in 2015, and he needed to raise cash to pay for home repairs, he could decide which "inventory" to sell from. Selling the 2006 shares would generate a much larger capital gains tax cost than selling the 2015 shares; the tax cost would drive which shares he picked.

Too bad for Grandaddy: the bill the Senate passed (section 13533) removes this choice and requires that whatever shares were purchased first get applied to any sale (first-in-first-out). Taxes for him, and millions of other individual investors will rise. Investors in mutual funds could be particularly hurt.

No such constraints are being put on the oil industry -- even though the International Financial Reporting Standards (IFRS) have not allowed LIFO for many years. Though pressure has been building for the US firms to comply with international standards, for now LIFO is still allowed in corporate accounting. US accounting rules do require firms to track the difference between the first-in-first-out method required internationally and the tax-favored LIFO approach via a line item called the "LIFO Reserve." This data allows one to see which firms and industries are benefiting most from LIFO accounting: the bigger the reserve, the more the firm is saving. Privately-held firms can also benefit from this, but there is no public data to see the resultant amounts.

Available data illustrates that some of the biggest beneficiaries of LIFO are the oil industry. Using data from Moody's Investor Services, CFO Magazine estimated that in 2010, that two thirds of the LIFO reserve for the energy sector was ExxonMobil alone; and that the energy sector comprised 37% of the total LIFO reserve for all public firms.

More recent data on the energy sector shows that the beneficiaries of LIFO are highly concentrated, still dominated by Exxon Mobil (see Table 1).

Table 1. LIFO Reserve (2008-2015) in Millions

Company

2008

2009

2010

2011

2012

2013

2014

2015

EXXON MOBIL CORP

10,000

17,100

21,300

25,600

21,300

21,200

10,600

4,500

CHEVRON CORP

9,368

5,491

6,975

9,025

9,292

9,150

8,135

3,745

VALERO ENERGY CORP

686

4,500

6,100

6,800

6,700

6,900

857

790

IMPERIAL OIL LTD

812

1,509

1,857

2,160

1,769

1,680

739

309

WESTERN REFINING INC

26

126

174

214

148

194

28

198

CALUMET SPECIALTY PRODS-LP

28

30

56

88

38

32

19

41

UNITED REFINING CO

153

5

50

92

78

109

110

6

CONOCOPHILLIPS

1,959

5,627

6,794

8,400

200

160

6

6

ALON USA ENERGY INC

4

100

115

93

58

61

8

1

HESS CORP

500

815

995

1,276

1,123

339

-

-

HOLLYFRONTIER CORP

33

207

284

378

134

273

-

-

MURPHY OIL CORP

202

551

735

580

571

269

-

-

Total

23,771

36,061

45,435

54,706

41,411

40,367

20,502

9,596

Source: June Li and Megan Y. Sun, "LIFO Distortion in the Oil Industry – Revisited," Accounting and Finance Research, V. 6, No. 3; 2017.

1In his extensive article on the role of boosting flow in pushing for drilling in ANWR, Philip Wight notes that "In 1970, M.A. “Mike” Wright, the CEO of Humble Oil (soon to be renamed Exxon), delivered extemporaneous remarks to a government task force and offered a rare glimpse of the oil industry’s plans for Arctic development. Wright explained that the industry committed to a 48-inch-diameter pipeline in part because it anticipated drilling offshore in the Arctic Ocean and restricted onshore areas, including the Arctic National Wildlife Refuge. Production from these areas would be necessary to realize the pipeline’s optimum daily flow. Wright’s statements were not only the first public announcement that the oil industry wanted to drill in ANWR, but a revelation that the pipeline’s design was intimately tied to extracting oil from it."

If a company or an industry is going to get subsidized, there are good ways and there are better ways for it to happen if one is sitting in the corporate suite. Among the best is to receive big subsidies that, while not flowing to your competitors, arrive in a form that nobody seems to notice. The benefits of this structure are clear: while the recipient gets a large slug of financial support, because few people see or understand the largesse, the political cost to both obtain and retain the subsidy is relatively low. Master Limited Partnerships, the subject of Earth Track's most recent report Too Big to Ignore: Subsidies to Fossil Fuel Master Limited Partnerships, prepared for Oil Change International, fit the bill here perfectly:

They are big. Not only can beneficiary companies with hundreds of billions of dollars in market cap entirely escape corporate income taxes on profits earned from eligible activities, but they can also defer for many years any tax payments on the gobs of cash they distribute out to their owners.

They are mostly hidden. Energy subsidy studies documenting tax breaks conducted in recent years by the US Department of Energy, the Congressional Budget Office, the US Treasury, and the Government Accountability Office have either not mentioned MLP subsidies at all, or done so only in passing with no related numerical estimate. The Congressional Research Service did mention the tax break, but did not link it to energy. Only the Joint Committee on Taxation (JCT) both linked the tax break to energy and included an estimated revenue loss figure. Unfortunately, JCT's first estimates came only in 2008, though fossil fuel MLPs were already surging in earlier years.

They are selective. Because most industries can't partake in this little game, the tax exemption for MLPs generates an especially big market boost to oil and gas over other energy options. Nearly every other industry lost their ability to form tax-favored publicly-traded partnerships like MLPs in 1987, more than a quarter-century ago. The reason? Congress was afraid corporate income tax revenues would be gutted. Since that time, fossil fuels have increasingly dominated this tax break, comprising well more than 75% of the sector by 2012.

They have (until this point) little political risk. Fossil fuel MLPs continue to grow very quickly, and, unlike common and highly visible subsidies to wind and solar, MLP tax breaks never expire.

Selective Subsidies That Work Counter to National Fiscal and Environmental Goals

MLP tax expenditures are part of a broader set of government subsidies that continue to underwrite activities contributing to climate change. These policies not only have large fiscal costs, but also work counter to the country's environmental goals and our national interest.

Fossil fuel MLPs are growing quickly. The market capitalization of fossil fuel MLPs reached an estimated $385 billion by the end of March 2013, up from less than $14 billion in 2000. Related tax subsidies have been as high as $4 billion annually in recent years at the federal level alone. Because the tax benefits from MLPs also ripple through state income tax codes, the combined state and federal MLP subsidies would be even higher.

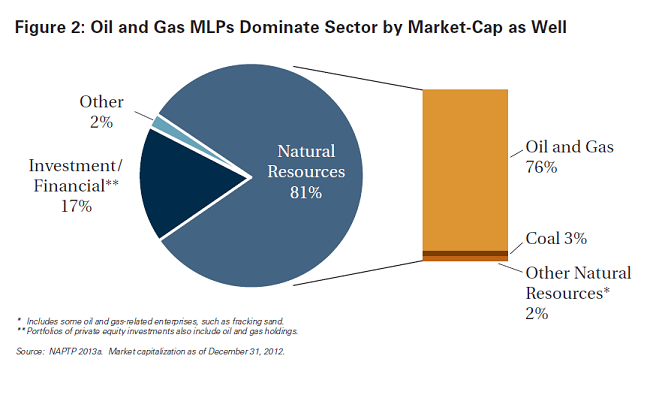

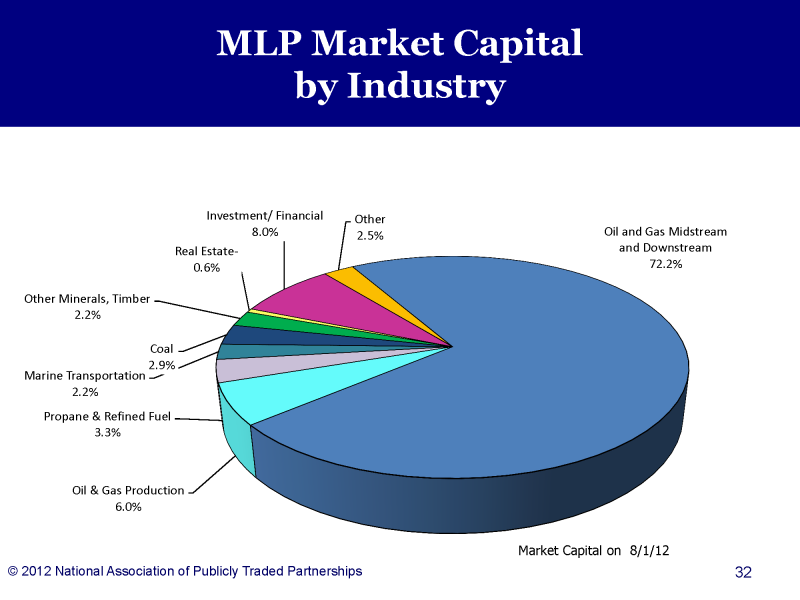

Fossil fuel activities continue to dominate MLPs, both in number of firms and share of total market capitalization. As of the end of last year, 77 percent of MLPs were in the oil, gas, and coal sectors based on data collected by the National Association of Publicly Traded Partnerships (NAPTP), the main industry trade association. Firms in the fossil fuel sectors comprised 79 percent of total MLP market capitalization, though this figure is likely a bit low. Firms classified in other sectors also include some oil and gas-related businesses, including fracking sand and fossil fuel investments held by publicly-traded private equity firms such as Blackstone.

MLP Subsidies to Fossil Fuels: Underestimated and Ignored for Too Long

Government estimates of tax expenditures from energy-related MLPs are too low. Tax expenditures related to MLPs have been understated in recent years, and appear to be growing rapidly. Using a variety of estimation approaches, we estimate that tax preferences for fossil fuel MLPs cost the Treasury as much as $13 billion over the 2009-12 period, more than six times the official estimates.

MLP tax breaks are among the largest subsidies to fossil fuels. Although most government reviews of energy subsidies have not even included MLP-related tax expenditures, our estimates suggest this subsidy is among the top five largest fiscal subsidies to the fossil fuel sector and the largest single tax break to the sector.

Growing share of production cycle for oil, gas, and coal can be organized as a tax-favored MLP - indicative that revenue losses will continue to grow. Financial innovation and IRS private letter rulings have expanded the fossil fuel market segments able to legally and successfully operate as tax-favored MLPs. Recent innovations have even established a precedent by which MLPs have successfully acquired taxable corporations, taking them off the corporate tax role in the process.

MLPs for All? Providing Matching Tax Breaks to Renewables May Not be a Panacea

Though supported by many environmental groups, recent legislation introduced to expand MLP-eligibility to a range of new energy technologies may not be the panacea it is widely believed to be by supporters. Further, the legislation is currently worded to include a range of energy technologies such as waste-to-energy, landfill gas, coal-to-liquids, and biomass that have a decidedly mixed environmental profile.

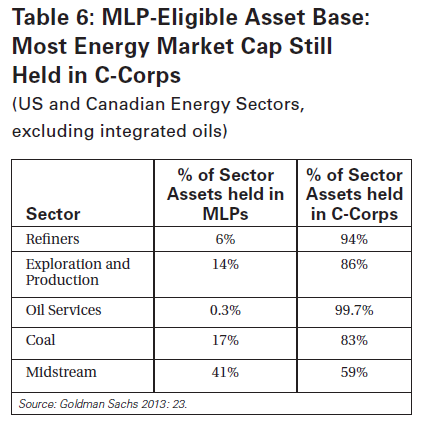

Even in well-established market segments, there is a large overhang of fossil fuel assets poised to exit the corporate income tax system through conversion to MLPs. Less than 20 percent of total assets in the refiners, exploration and production, oil services, and coal sectors are presently held in a tax-favored MLP format (see Table). Even in the MLP-intensive midstream segment of the oil and gas market, conventional (taxable) corporate forms continue to own more than half of the assets. In all of these sectors, there is a huge pool of assets that multiple investment firms anticipate will convert to MLPs in coming years.

Proposed expansion of MLP eligibility to renewables risks disproportionate benefits flowing instead to the fossil fuel sector. Current efforts to expand MLP treatment to renewables (The Master Limited Partnerships Parity Act) may entrench existing subsidy recipients. The expansion will reduce the likelihood that MLP's tax-exempt treatment will be ended for fossil fuel producers, allowing the rapid growth of tax-exempt fossil fuel MLPs to continue unchecked. This legislation also would open MLP-eligibility to power generation for the first time, creating risks that this treatment will be extended from the current proposed set of recipients (biomass, solar, wind, geothermal) to all forms of power generation in coming years. This would disadvantage energy conservation, offset hoped for gains from the expansion in renewable sectors, and trigger very large tax losses to Treasury.

MLP Subsidy Termination a More Logical Path than Further Expansion

The MLP loophole should be closed; MLPs should be taxed as conventional corporations, not extended to new uses. This strategy, continuing what the United States started in 1986, would eliminate large and growing subsidies to fossil fuels. Canada also successfully ended tax-favored treatment of an equivalent corporate structure in 2006. In both cases, the affected industries did not wither and die; they adapted and moved on. This newest crop of tax-favored fossil fuel firms will do the same.

Special legislative provisions have allowed a select group of industries to operate as tax-favored publicly-traded partnerships (PTPs) more than 25 years after Congress stripped eligibility for most sectors of the economy. These firms, organized as Master Limited Partnerships (MLPs), are heavily concentrated in the oil and gas industry. Selective access to valuable tax preferences distorts energy markets and creates impediments for substitute, non-fossil, forms of power, heating, and transport fuels.

Master Limited Partnerships (MLPs) are a special corporate form, used primarily by natural resource industries. They enable firms to both raise capital on public equity markets and to pay zero corporate income taxes. MLPs deserve far more scrutiny as energy subsidies than they have received to date. Although the US Energy Information Administration (EIA) excluded them from their most recent study of US energy subsidies on the grounds that other industries also benefit (so the subsidies are not "energy-specific"), EIA's logic is weak. Based on data compiled by the National Association of Publicly Traded Partnerships in August 2012, roughly 87% of the total market capitalization of the MLP sector was associated with fossil-fuel related activity. That's pretty focused.

And the dollars look to be large -- between $5 and $15 billion/year in revenue losses, funds that either increase our deficit or have to be made up through higher taxes on other taxpayers. More precise review of data on specific MLPs would be needed to tighten this range. But even at the low end, tax subsidies through MLPs alone generate higher subsidies to fossil fuels than everything else that EIA counted combined. Let's just say that the government's subsidy figures are highly sensitive to which policies they ignore.

With enormous pressure on Congress to identify ways to boost revenues and reduce economic distortions from the tax code, stripping the tax exemption of MLPs seems a great place to look. Of course the industry will lobby heavily to protect their subsidy; it always does. But elimination is still good public policy. In fact, were the industry to argue that the world will end if MLP tax treatment changes, we can point out that Canada has already traveled this path. In 2006, Canada eliminated preferential tax treatment for their energy investment trusts, a corporate structure modeled on, and analogous to, MLPs. And the oil and gas industry did not disappear.

The remainder of this blog is extracted from a more detailed review I did on subsidies that the Romney presidential campaign forgot when it discussed energy subsidies.

With all of the talk this campaign season about reducing income tax burdens on small business, it is easy to forget that an ever higher percentage of small businesses (and many larger ones) are adopting corporate forms that escape corporate income taxes entirely. This includes sub-S corporations, partnerships, and limited liability corporations. As a result, the share of national income paid from corporate income taxes has dropped from nearly 30% in the 1950s to less than 11% for the period 2000-2009.[1] But one group of enterprises - those raising capital on public equity markets - must generally still use corporate forms that pay corporate taxes.

One glaring exception is publicly-traded partnerships (PTPs), also known as Master Limited Partnerships (MLPs). Under special rules, this group of companies can both raise capital on public markets and bypass corporate income taxes entirely. Tax liabilities (and enterprise-related subsidies) pass directly out to the partners' individual tax returns. MLPs don't make up a huge chunk of listed firms on the stock market. But within the tax favored MLP universe, oil and gas companies dominate, including a new one focused on fracking sand.

One other sector able to use the MLP approach is also relevant to this debate: private equity firms. If Bain Capital (the firm that Mr. Romney founded) wanted to go public so partners could cash in their built-up equity, they would likely become an MLP. Blackstone and KKR, two large private equity firms, have already done so.

Table: Avoided taxes on oil and gas MLPs alone exceed totals subsidies DOE attributed to the sector

$293b/yr

Market capitalization of fossil fuel-related MLPs, as of August 2012.[2] The MLP corporate form allows many oil and gas operations to both raise capital on public stock markets and pay no corporate-level income taxes.

$20-56b/yr

Estimated income generated by fossil fuel MLPs, based on reported yields. This income entirely escapes corporate taxation.[3]

$5-15b/yr

Estimated tax savings to fossil fuel sector from using an MLP relative to a standard corporation, based on assumptions on tax rates by the National Association of Publicly Traded Partnerships.

87%

Share of all MLPs, by market capitalization, in the fossil fuel sector.

$0

Subsidies associated with MLPs that the US Energy Information Administration captures in its evaluations, excluding it on the basis that "the tax treatment of PTPs is not exclusive to the energy sector."[4]

1.8 - 5.4

Tax subsidy to fossil fuel MLPs as a multiple of all subsidies to oil and gas EIA counted in its 2011 analysis.

[1] Chuck Marr and Brian Highsmith, "Six Tests for Corporate Tax Reform," Center for Budget and Policy Priorities, 24 February 2012. [2] National Association of Publicly Traded Partnerships, "Master Limited Partnerships 101: Understanding MLPs," August 2012. [3] Low-end assumes a yield of 6.7%, the average of fossil-fuel-related MLPs based on MLPs listed on the Yield Hunter website with additional data from Google Finance. High-end estimate is from Telis Demos and Tom Lauricella, "Yield-Starved Investors Snap Up Riskier MLPs," Wall Street Journal, 16 September 2012. [4] U.S. Energy Information Administration, Direct Federal Financial Interventions and Subsidies in Energy in Fiscal Year 2010, 2011, p. x.

Even in well-established market segments, there is a large overhang of fossil fuel assets poised to exit the corporate income tax system through conversion to MLPs. Less than 20 percent of total assets in the refiners, exploration and production, oil services, and coal sectors are presently held in a tax-favored MLP format (see Table). Even in the MLP-intensive midstream segment of the oil and gas market, conventional (taxable) corporate forms continue to own more than half of the assets. In all of these sectors, there is a huge pool of assets that multiple investment firms anticipate will convert to MLPs in coming years.

Even in well-established market segments, there is a large overhang of fossil fuel assets poised to exit the corporate income tax system through conversion to MLPs. Less than 20 percent of total assets in the refiners, exploration and production, oil services, and coal sectors are presently held in a tax-favored MLP format (see Table). Even in the MLP-intensive midstream segment of the oil and gas market, conventional (taxable) corporate forms continue to own more than half of the assets. In all of these sectors, there is a huge pool of assets that multiple investment firms anticipate will convert to MLPs in coming years.

{kind=link}